25% of consumers recently used a buy now, pay later loan, report finds

Hey Payments Fanatic!

As "buy now, pay later" (BNPL) programs gain popularity, many shoppers are turning to this payment structure to manage their finances.

According to the Federal Reserve Bank of New York, Americans collectively owe $17.5 trillion in various debts, including credit cards, mortgages, and auto loans, with $1.12 trillion specifically on credit cards.

BNPL loans, often not appearing on credit reports, create a kind of “phantom debt” that remains unaccounted for in these totals.

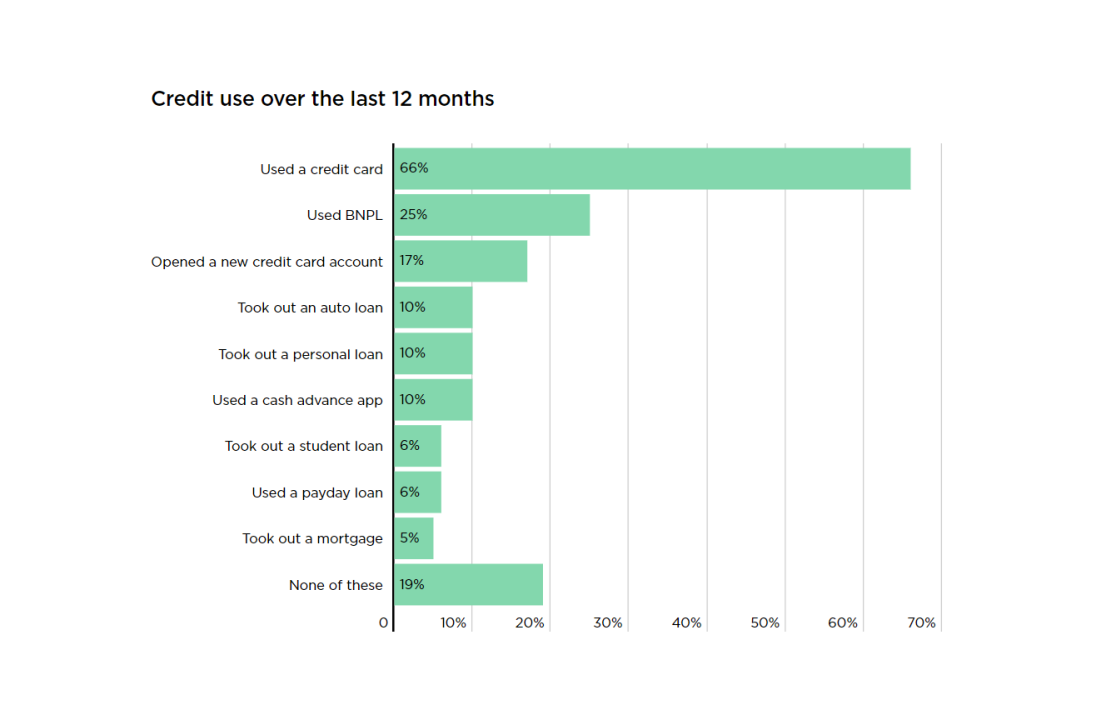

A recent report by NerdWallet highlights that BNPL plans are now the second-most used credit payment method among U.S. consumers.

Credit cards are still the most commonly used form of credit, with 66% of respondents using them in the past 12 months.

Cheers,

PAYMENTS NEWS

🇲🇽 Viva.com, Nexi, and MyPos to Offer Tap to Pay on iPhone for Merchants in Italy. Tap to Pay on iPhone allows merchants to accept contactless payments, including credit and debit cards, Apple Pay, and other digital wallets, using just an iPhone and the Viva.com app, Nexi SoftPOS app and the myPOS Glass app, respectively, with no extra hardware needed.

🇱🇺 Worldline signs deal with Banque Raiffeisen for cloud based instant payments. Worldline will enable Banque Raiffeisen to send and receive instant payments as mandated by the EU's Instant Payments Regulation. Using Worldline’s modern cloud infrastructure, the bank will benefit from smarter and quicker onboarding processes.

🇨🇳 Pyvio selects Currencycloud to deliver cross-border payments for Chinese merchants. The partnership will allow Pyvio to leverage Currencycloud’s technology to collect and pay funds in over 180 countries and more than 30 currencies, including CNH and CNY.

🇬🇧 Currencycloud selects Form3 for Confirmation of Payee. The Form3 Confirmation of Payee Requester Service enables Currencycloud’s customers to verify account holder and payee details to provide fast and secure account verification.

🇲🇿 Flutterwave Mozambique receives payment aggregator license approval in principle. This license enables Flutterwave to offer its comprehensive payment services within Mozambique and strengthen its operations in southern African markets.

🇺🇾 Totalnet Uruguay has officially launched its new mobile app. This app turns Android phones with NFC capabilities into point-of-sale (POS) terminals, allowing merchants to accept card payments easily, quickly, and securely. Designed especially for small businesses and entrepreneurs, this tool promises.

🇺🇸 The web3 payments firm Coinflow Labs raised $2.25 million in seed funding. Coinflow develops a payment system that instantly accepts payments and settles transactions with stablecoins. The platform also allows businesses to send funds from stablecoins to a user's bank account immediately.

GOLDEN NUGGET

What is Payment Routing?

Below is a diagram made by Ali Ahmed of 9️⃣ potential routing logics you might encounter. 👇

Let’s dive in:

Payment routing is apart of the Payment process for merchants working with multiple PSPs.

The idea is that, based on a set of rules decided by the merchant, transactions will take the most efficient path to the right PSP.

There are 2 types of routing, static & dynamic.

1️⃣ Static Routing: Static routing is when a merchant delivers transactions to a PSP through a route they manually configured. The path of the transaction is set in stone & can't "intelligently" make the right decision.

2️⃣ Dynamic Routing: Dynamic payment routing is able to adjust the path of the transaction in real-time, based on current conditions. It's sometimes called "smart" or "intelligent" routing since it can make decisions based on logical rules, rather than a set path.

What are the benefits of dynamic routing?

► Resilience - Transactions can be rerouted if a path or node in the network goes down.

► Scalability - As payments become more complex, dynamic routing allows merchants to remove the burden of taking on more transactions than normal. Companies that are growing internationally (like Dollar Shave Club) benefit.

► Cost Effectiveness - Dynamic routing ensures that the lowest costly route is picked, meaning transaction fees are always lower on average.

► Load Balancing - To prevent congestion, or simply to fulfill volume metrics, dynamic routing can more evenly distribute transaction traffic across its existing network. Some high-risk merchant providers (like PaymentCloud) benefit here.

► User Experience - Faster transaction times, lower fees on average, & reduced likelihood of failed transactions mean that consumers don't experience friction, while merchants optimize revenue.

Should merchants build a dynamic payment routing system in-house, or use a provider? This question comes up a lot.

Long-term, an in-house dynamic routing system makes it hard to remain efficient & scalable.

Each new alternative payment method can take 2-4 weeks to integrate, each payment method or rail can have different fees, & issue handling takes longer.

By using a provider, like ACI Worldwide for example, adding new payment methods to routing is like turning on a light switch, there's only one fee for all payment methods & provider rails, and issue handling can be taken care of in minutes.

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn.

Comments ()