A Nexi Takeover?

Hey Payments Fanatic!

Private equity firm CVC is eyeing an early-stage takeover of Nexi, valuing the company at around €9 billion ($10.5 billion), marking its third attempt after prior explorations.

Nexi, a key player in merchant solutions and card issuing across Europe, has seen its shares drop 65% over four years amid fee pressures, contract renegotiations, and FinTech competition.

The bid sparked a 19% intraday surge in Nexi's stock, pushing its market cap toward $9.4 billion temporarily.

Italy's "golden power" rules could block the deal, as Nexi is viewed as critical financial infrastructure, potentially requiring a carve-out of its digital banking unit to a state-backed entity like Cassa Depositi e Prestiti.

CVC envisions transforming Nexi into a software-focused firm, but regulatory and political scrutiny in Rome looms large, with Nexi's €6 billion debt adding complexity.

Will CVC crack Italy's defenses, or is this déjà vu for the unicorn turned target?

Discover the rest of the payments’ big shifts below. See you tomorrow!

Cheers,

INSIGHTS

📈 Checkout.com just joined Stripe and Adyen as a "Leader" in Forrester’s 2026 report in the Merchant Payments Providers category.

NEWS

🇮🇹 CVC weighs €9bn bid for Italian payments group Nexi after a sharp share price decline, though any deal would depend on support from the Italian government due to political sensitivities and control of financial infrastructure. Read more

🌎 Tether leads Belo's $14 million raise to expand stablecoin payments across Latin America. By combining payments, foreign exchange, and cross-border transfers in one app and relying on stablecoin infrastructure, Belo aims to lower costs and friction in Latin America’s fragmented financial systems and serve users underserved by traditional banks.

🇫🇷 Worldline completes divestments and revenues beat expectations. The divestment programme aims to streamline Worldline's cumbersome portfolio of businesses and help it return to growth. Worldline is now worth only a fraction of the market value it had at its pandemic peak.

🇺🇸 Corpay launches AI capabilities to modernise spend management. These innovations bring practical, high-impact AI into everyday financial workflows to help companies move faster, reduce manual work, and make more informed decisions. Keep reading

🇺🇸 Sokin and Adyen partner to give US businesses a single solution for ecommerce payments and treasury operations. Businesses can accept payments through Sokin’s checkout and payment links functionality across more than 35 payment methods, over 170 countries and territories, and charge and settle in multiple currencies.

🇺🇸 Square brings Managerbot to more sellers, giving Main Street an intelligent business agent. Managerbot provides sellers with a powerful, proactive tool that monitors operations, surfaces insights, automates routine tasks, and protects their businesses.

🇬🇧 LemFi announces a £100 million commitment to the UK economy and establishes London as our Global Headquarters. The investment will support hiring, technology development, and compliance infrastructure, reinforcing the company’s global growth and its role in cross-border financial solutions.

🇺🇸 SumUp expands its core product ecosystem to empower millions of U.S. small businesses. The company’s product lineup brings together everything a business needs under two clear pillars: Run Your Business and Take Payments. These updates give merchants a clearer picture of their business, and more control over how they grow it.

🇭🇰 ZEN.COM secures Hong Kong license. The MSO license enables ZEN.COM to expand its financial services in the region and further strengthen relationships with global partners, particularly in e-commerce and cross-border payments. Continue reading

🇺🇸 Bloxley partners with Equals Money | Railsr to power European financial infrastructure. Through the partnership, Bloxley will integrate Equals Money's multi-currency account capabilities, international payment rails, and enterprise-grade security features into its platform, creating reliable, compliant, modern payment experiences for its customers.

🇺🇸 Innovative Payment Solutions has partnered with FINAP Worldwide to form FINAP USA, a jointly owned entity that will commercialise integrated banking and payments platforms across North America. The venture combines IPSI’s U.S. infrastructure with FINAP’s global technology to expand into high-growth FinTech sectors.

🌏 Thunes and WireBarley launch real-time payment solution for 1.1 million users across Asia and Beyond. By integrating with Thunes’ Direct Global Network, WireBarley’s 1.1 million users gain access to enhanced payout capabilities and faster remittance services across seven sending countries and 520 payout corridors.

🇳🇬 MTN Group to acquire 60% stake in MTN Nigeria’s MoMo and Y’ello Digital for N95bn. The move aims to consolidate ownership under a new holding structure while reducing MTN Nigeria’s exposure to loss-making FinTech operations.

🇬🇧 Airtel targets $2bn London IPO for mobile money unit. The listing would be a boost for the LSE, which has recently seen local FinTechs such as Klarna, Wise, and Revolut either pick or at least explore New York for IPOs. Read more

🇱🇹 YamSoft launches AI-powered payment capabilities following €2.35M EU innovation grant. The grant has enabled YamSoft to develop and deploy advanced AI capabilities now available to payment service providers and FinTech operators across Europe.

🇬🇧 CAB Payments Non-Executive Director Kushagra Saxena to step down. Saxena is stepping down from the board to take up an executive position at another organisation. During his time on the board, Saxena advised the company across a range of strategic areas, including its digital, technology, and stablecoin strategies.

🇺🇸 Visa accelerates stablecoin momentum. Visa has expanded its stablecoin settlement pilot by adding five new blockchains, Base, Canton, Polygon, Tempo, and Arc, bringing total support to nine networks. The move strengthens Visa’s multi-chain strategy as stablecoin settlements scale, reaching a $7 billion annualised run rate.

🇺🇸 MoneyGram modernises retail solutions globally with Stripe, advancing a unified, omnichannel experience. The launch upgrades its global retail footprint with a modern payments infrastructure and the best point-of-sale technology in the industry.

GOLDEN NUGGET

OpenAI'𝐬 𝐚𝐠𝐞𝐧𝐭𝐢𝐜 𝐜𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐬𝐡𝐢𝐟𝐭 — 𝐚𝐧𝐝 𝐰𝐡𝐚𝐭 𝐢𝐭 𝐦𝐞𝐚𝐧𝐬 𝐟𝐨𝐫 𝐦𝐞𝐫𝐜𝐡𝐚𝐧𝐭𝐬 👇Created by Arthur Bedel 💳 ♻️

OpenAI just quietly redefined how #AgenticCommerce will work.

The shift is not getting the attention it deserves.

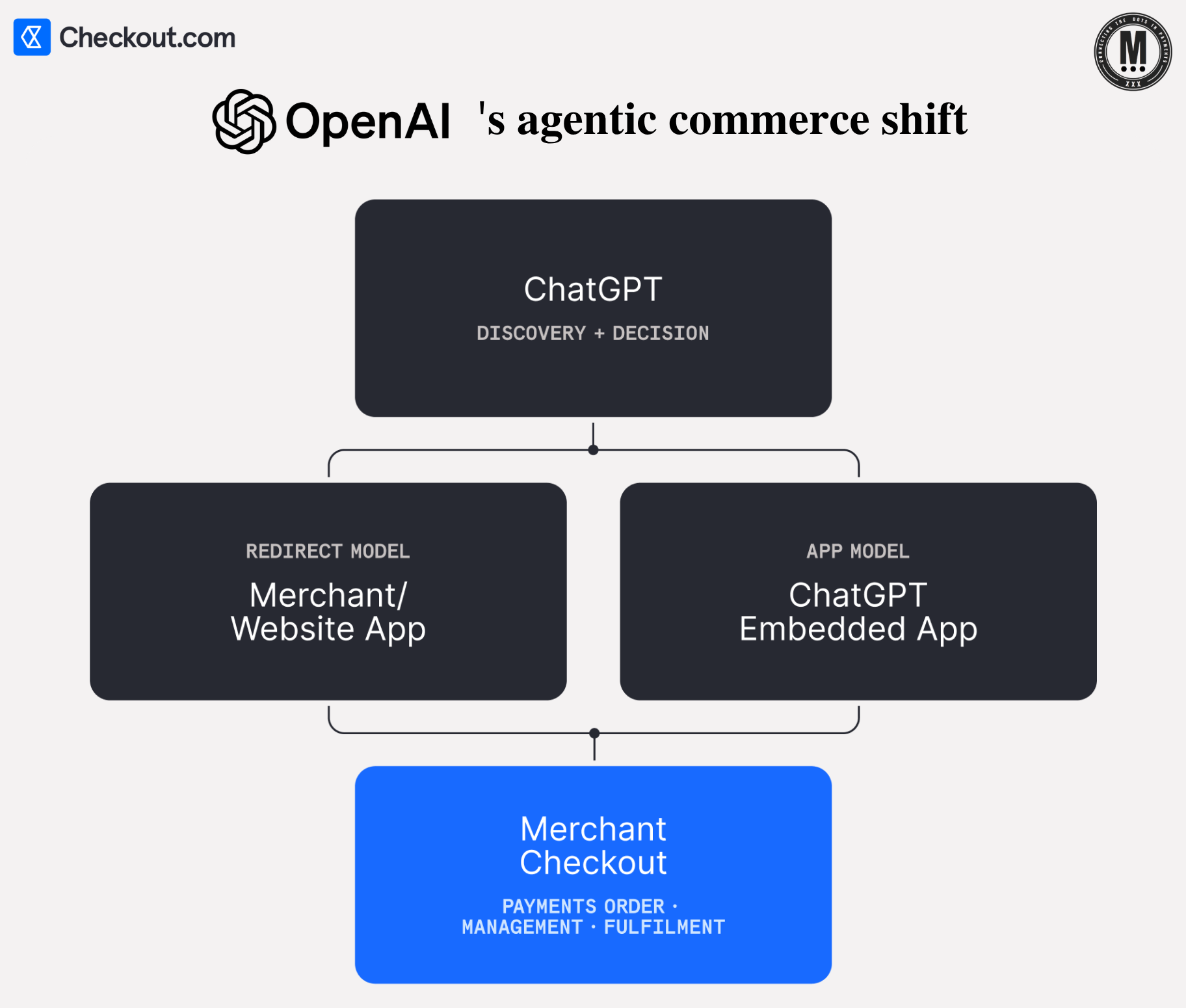

𝐂𝐡𝐚𝐭𝐆𝐏𝐓 𝐢𝐬 𝐦𝐨𝐯𝐢𝐧𝐠 𝐚𝐰𝐚𝐲 𝐟𝐫𝐨𝐦 "𝐈𝐧𝐬𝐭𝐚𝐧𝐭 𝐂𝐡𝐞𝐜𝐤𝐨𝐮𝐭" — where purchases were completed directly inside the chat — and toward merchant-controlled checkout models.

Some are calling this a retreat from in-chat commerce.

It is not.

It is the opposite. It is the moment AI becomes the new shop window — while merchant infrastructure remains the system of record.

Here is what is actually changing.

Instead of completing purchases entirely inside ChatGPT, transactions are now moving into merchant-controlled environments through two primary models.

The first is the redirect model.

The shopper discovers and decides in ChatGPT, then gets guided to the merchant's website or mobile app to complete the purchase.

The second is the app model.

Merchants build dedicated experiences inside ChatGPT using OpenAI's SDK — with checkout powered by their own infrastructure via delegated #Payments flows.

In both cases, the principle is the same: the merchant owns the checkout, not the AI platform.

This positions OpenAI's Agentic Commerce Protocol as an enablement layer — not a marketplace intermediary sitting between the merchant and the transaction.

Why does this matter?

Because checkout is deeply tied to merchant-specific realities — inventory, fulfillment, loyalty, regional #APMs, compliance, and customer account systems.

None of these are easily abstracted into a universal AI interface.

What is emerging is not AI-owned commerce.

It is AI-orchestrated commerce — where intent is generated in one layer and executed in another.

For merchants, the foundations remain the same: delegated payments, tokenized credentials, high-quality product data, and flexible API-driven checkout.

What is changing is how customers arrive.

Increasingly, purchase intent will be formed before a shopper ever reaches a merchant's owned channels. AI assistants will act as a qualification layer — narrowing options, shaping preferences, accelerating decisions.

The merchants who win will be the ones who can do two things at once: surface effectively inside AI-driven discovery, and convert seamlessly when that demand is routed to them.

And here is the bigger picture.

OpenAI's ACP. Google's Universal Commerce Protocol. The card networks' own frameworks. They are all solving the same problem from different angles — and fragmentation will persist in the near term.

The merchants who stay flexible across multiple models will be the ones capturing the opportunity.

The era of #Fintech where AI controls discovery and merchants control conversion is just beginning.

Which model do you think will win — redirect or embedded?

Source: Checkout.com

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()