BNPL Giants Turn to Securitization for New Funding

Hey Payments Fanatic!

FinTech Companies offering buy now, pay later (BNPL) services, such as PayPal, and Klarna, are leveraging debt backed by consumer loans to find new funding methods in a higher interest rate environment.

By offering pools of assets repackaged as securities, these firms can access relatively inexpensive funding through private markets. This strategy, according to several lawyers and bankers at the Global ABS conference in Barcelona, is driving a resurgence in the sector.

PayPal recently signed an agreement with private equity firm KKR & Co. to sell its European loan packages. Similarly, Klarna has secured comparable debt in private deals, according to sources familiar with the transactions, although a representative for Klarna declined to comment.

Other companies are also using securitization deals to fund their operations. US-based Affirm, known for facilitating purchases of Peloton bikes, sold approximately $2.4 billion in asset-backed securities (ABS) last year. Australia's Zip Co. has also been active in the market, issuing A$3.1 billion ($2.1 billion) overall.

The buy now, pay later model, which allows consumers to spread out payments interest-free, faced scrutiny in 2022 as central banks began raising borrowing costs from historic lows. However, the use of securitization might provide a crucial lifeline for the sector, provided that default rates remain manageable.

Have a great start to the week and I'll be back in your inbox with more updates tomorrow!

Cheers,

PAYMENTS NEWS

🇲🇳 Khan Bank partners with Alipay+ for cross-border mobile payments in Mongolia, integrating 12 international e-wallets from eight countries and regions for seamless digital transactions. Read more

🇵🇰 1LINK, in partnership with Raast, an initiative by the State Bank of Pakistan (SBP), and 13 merchant aggregators, has launched the 1GO Raast Person to Merchant (P2M) service. The 1GO Raast P2M service aims to transform the landscape of interoperable P2M payment services in Pakistan. The service includes a range of features such as Dynamic QR Code, Static QR Code, Request to Payment Now & Later, and Bulk Request to Payment Later Processing.

🇬🇧 A UK tribunal has ruled that interchange fee lawsuits against Visa and Mastercard can proceed. The two US giants are being sued on behalf of hundreds of merchants over the multilateral interchange fees charged for accepting card payments. Read more

🇲🇾 Malaysians will soon be able to make QR payments in South Korea using the Paybooc app, thanks to a collaboration between Korea’s BC Card and Malaysia’s PayNet. Starting this month (June), the first phase of this collaboration enables South Koreans to make QR payments in Malaysia using the BC Card e-wallet app.

🇺🇸 Utah-based healthcare payments software company Waystar envisions $20B healthcare payments market. The software provider is attempting to build its software business by simplifying a complex web of payments for healthcare providers and patients.

🇺🇸 Till Payments – a subsidiary of Nuvei, partnered with BigCommerce to elevate online business payments. The partnership offers BigCommerce customers a feature-rich eCommerce payment solution, enabling seamless payment experiences for both online and in-store merchants through a single processing partner.

🇬🇧 Moneyhub, a data and payments platform, has announced the introduction of its account verification service. Powered by Open Banking, Moneyhub Account Verification enables better payment security utilising bank level security controls (including PSD2 SCA) and biometrics.

🇨🇦 FinTech firm Adyen has opened a new office in Toronto to anchor its Canadian operations and appointed Ilona Fagyas as Head of Sales. At Adyen, Ilona will focus on expanding the company's footprint in Canada and enhancing its commerce business.

🇺🇸 BNPL Company Zip Co. announces WNBA superstar Kelsey Plum as First Brand Ambassador. Together, they will spotlight Zip's commitment to providing accessible payment options that open doors to new experiences, events, and possibilities for customers across all economic backgrounds.

🇬🇧 UK-based payments solutions provider allpay Limited has announced a new partnership with issuer processing expert Enfuce. This collaboration aims to integrate secure cloud-based card payment solutions into the heart of public sector services, including local UK councils, impacting communities across the UK.

🇸🇦 Saudi Arabia’s central bank has joined the Bank for International Settlements’ (BIS) cross-border central bank digital currency (CBDC) project, mBridge, as a participant, after being an observing member.

🇬🇧 Sainsbury's agrees BNPL deal with Klarna to offer its payment methods at the online checkouts of three iconic brands: Argos, Habitat, and TU. Shoppers will be able to choose from Klarna's payment options: Pay Now, Pay Later in 30 days, or Pay in 3 equal installments.

🇨🇦 VoPay, in partnership with Avesdo, is set to modernize the pre-sale property market by introducing a fully embedded digital payment solution within Avesdo’s Transaction Management System (TMS). This partnership aims to eliminate the traditional inefficiencies that plague the home-buying process.

GOLDEN NUGGET

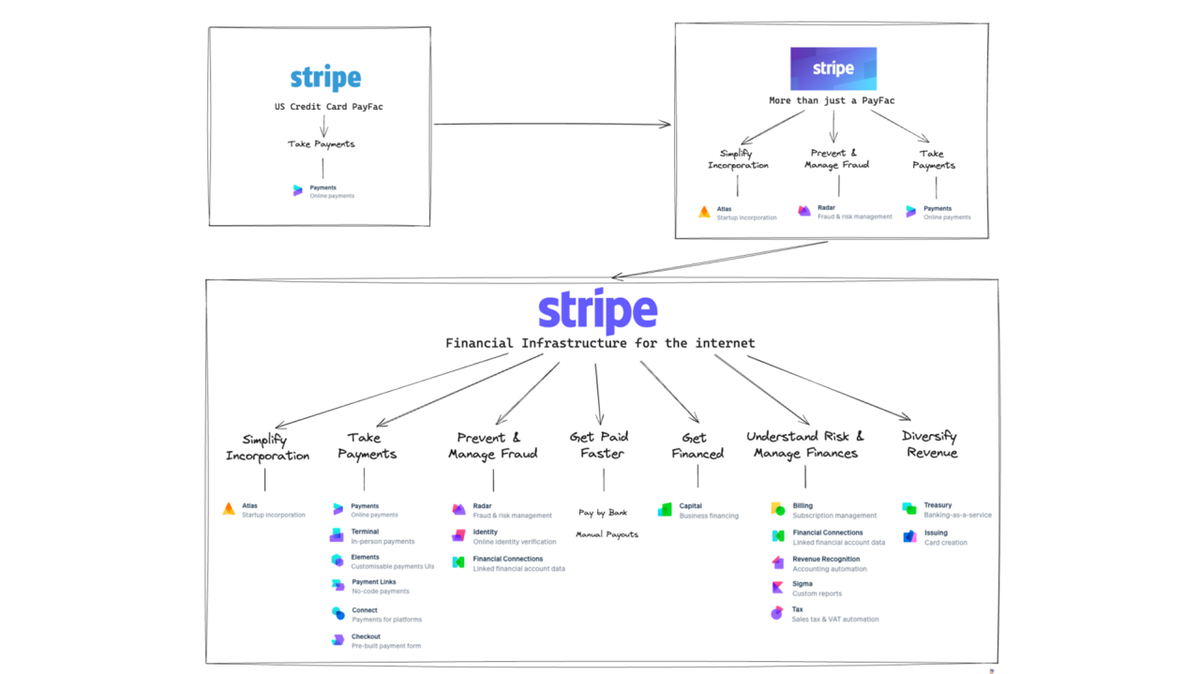

Stripe, founded in 2010 by Patrick and John Collison, has evolved from a basic Payments Facilitator into a multifaceted Financial Infrastructure platform.

Stripe was born out of the Collison brothers' frustration with complex payment systems. Inspired by SliceHost, a VPS hosting company known for its simplicity, Stripe offered a developer-friendly solution that allowed businesses to accept credit card payments with minimal code.

Leveraging their Y Combinator network, the brothers onboarded their first users from the YC alumni, gaining early traction and valuable feedback.

Stripe's offerings have significantly expanded over the years:

2011: Public launch with simple payment APIs.

2013: Stripe Connect for marketplace payments.

2015: Stripe Atlas for global business incorporation.

2016: Radar, a fraud prevention tool.

2020-2023: New products like Stripe Treasury and Stripe Climate, and international growth.

At recent events, Stripe announced several new products:

► Pay by Bank: Real-time bank transfers using the UK's Open Banking framework.

► Stripe Capital: Flexible financing for UK businesses based on transaction history.

► Radar Assistant: Custom fraud rule creation with a natural language interface.

► A/B Testing for Checkout: Simplified optimization of checkout experiences.

► Decoupled Products: Standalone use of Stripe Radar, Stripe Billing, and the optimized checkout suite, independent of Stripe’s payment processing.

Stripe’s growth has been driven by recognizing industry trends like mobile payments, demand for seamless user experiences, increased security focus, and global commerce.

Their developer-centric approach, transparent pricing, and full-stack solutions have resonated with the tech community.

Stripe focuses on several key metrics:

► Acquisition: Expanding through products like Atlas and interoperable solutions.

► Revenue: Enhancing customer revenue with tools like A/B testing and Stripe Capital.

► Retention: Improving with robust fraud prevention and seamless payments.

► Referral: Leveraging platforms like Connect for new customer acquisition.

Stripe’s journey provides key lessons:

1️⃣ Solve core problems with great products.

2️⃣ Identify and serve a core audience before expanding.

3️⃣ Embrace a tech-first approach with clear documentation.

4️⃣ Decouple core products for flexibility and market reach.

5️⃣ Monitor market trends for product evolution.

6️⃣ Address additional customer problems to capture more market share.

Conclusion:

Stripe's transformation from a Payments Facilitator to a financial infrastructure platform showcases strategic product development and market adaptation.

Their recent announcements strengthen their leadership in FinTech, offering a blueprint for other companies aiming to innovate and scale in the industry.

I highly recommend reading this deep dive article by Jas Shah for more info, and valuable lessons from Stripe’s journey so far.

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn.

Comments ()