Paysend Partners with BVNK to Expand Stablecoin Payments

Hey Payments Fanatic!

Paysend has partnered with BVNK to introduce stablecoin payments and settlement capabilities across its consumer and enterprise platforms.

For Paysend, the partnership represents a strategic step toward expanding its digital payments ecosystem and reinforcing its position in the cross-border payments market. For BVNK, it is an indicator of continued demand for stablecoin infrastructure.

Delivering trusted, scalable interoperability (connecting legacy systems, fiat, and multi-chain digital currencies) is now the critical priority.

Payment providers that master this integration early will gain a massive head start in the race to make tomorrow’s cross-border payments better, faster, and cheaper.

Last Wednesday, we covered Mastercard’s acquisition of BVNK, and today’s news is more proof that the industry’s biggest players are betting on hybrid finance.

Keep scrolling 👇 There’s more updates across the Payments landscape below. I will be back tomorrow in your inbox.

Cheers,

NEWS

🇮🇳 Mastercard promotes Rahul Agrawal to Engineering Leadership Role. In this expanded role, Rahul will lead software engineering strategy, platform development, and technology innovation initiatives, with a focus on building scalable, secure, and high-performance solutions to support Mastercard´s evolving global digital payment ecosystem.

🌍 Paysend partners with BVNK to expand stablecoin payments and cross-border settlement. By integrating stablecoin rails, Paysend aims to enhance the speed and flexibility of its global payments network, which already spans more than 170 countries and supports over 80 currencies.

🇺🇸 Venmo has expanded globally by integrating with PayPal, allowing users to send and receive money with PayPal users across 90 markets. The move simplifies international peer-to-peer payments using just a phone number, reducing friction and expanding Venmo’s reach to a global audience.

🇳🇬 Moniepoint acquires Orda Africa to enter Nigeria’s $19bn restaurant market. The deal folds Orda into Moniebook, Moniepoint’s point-of-sale and business management platform, giving the FinTech a direct play in a food service sector valued at $50 billion across the continent.

🇪🇹 M-PESA Ethiopia expands into tax collection with Amhara region deal. The agreement paves the way for the over 450,000 individuals and businesses across Amhara to pay taxes through M-PESA, which relies on in-person services that have historically entailed manual processing and multiple visits to revenue offices.

🇿🇦 Cape Town startup Happy Pay raises $5M seed round to scale the first ad-subsidized payments network, to deliver cost-free Buy Now Pay Later payments for SA consumers. The startup is building what it calls an ad-subsidized payments network, shifting the cost of instalments to the merchants and brands that actually benefit from the resulting sales.

🇹🇿 Visa supports digital payment innovation in Tanzania and Ethiopia. The new capability allows M-Pesa customers to make contactless payments using their Android mobile phones at any Visa-enabled point-of-sale terminal, both locally and internationally.

🇧🇷 BTG suspends Pix after hacker attack diverts R$ 100 million. The case adds to a series of breaches targeting third-party providers, underscoring increasing pressure on the ecosystem to strengthen real-time fraud detection and security measures.

🇮🇳 India and Bhutan collaborate on UPI-linked postal remittances. The initiative is designed to enhance financial connectivity and make digital remittance services more accessible to citizens in both countries. As part of the collaboration, the two countries signed a MoU, establishing a formal framework between India Post and Bhutan Post.

🇨🇦 Deloitte Canada and Stablecorp announce strategic collaboration on industry-first stablecoin infrastructure for Canadian financial institutions. Leveraging the inherent advantages of blockchain technology, speed, immutability, traceability, and efficiency will enable solutions that are robust, compliant, and scalable.

🌍 Cathay Pacific expands global partnership with Adyen. This expansion marks a significant milestone, with Adyen now providing direct acquiring services for the airline in markets including Hong Kong, Australia, New Zealand, the United States, Japan, and most recently, India.

GOLDEN NUGGET

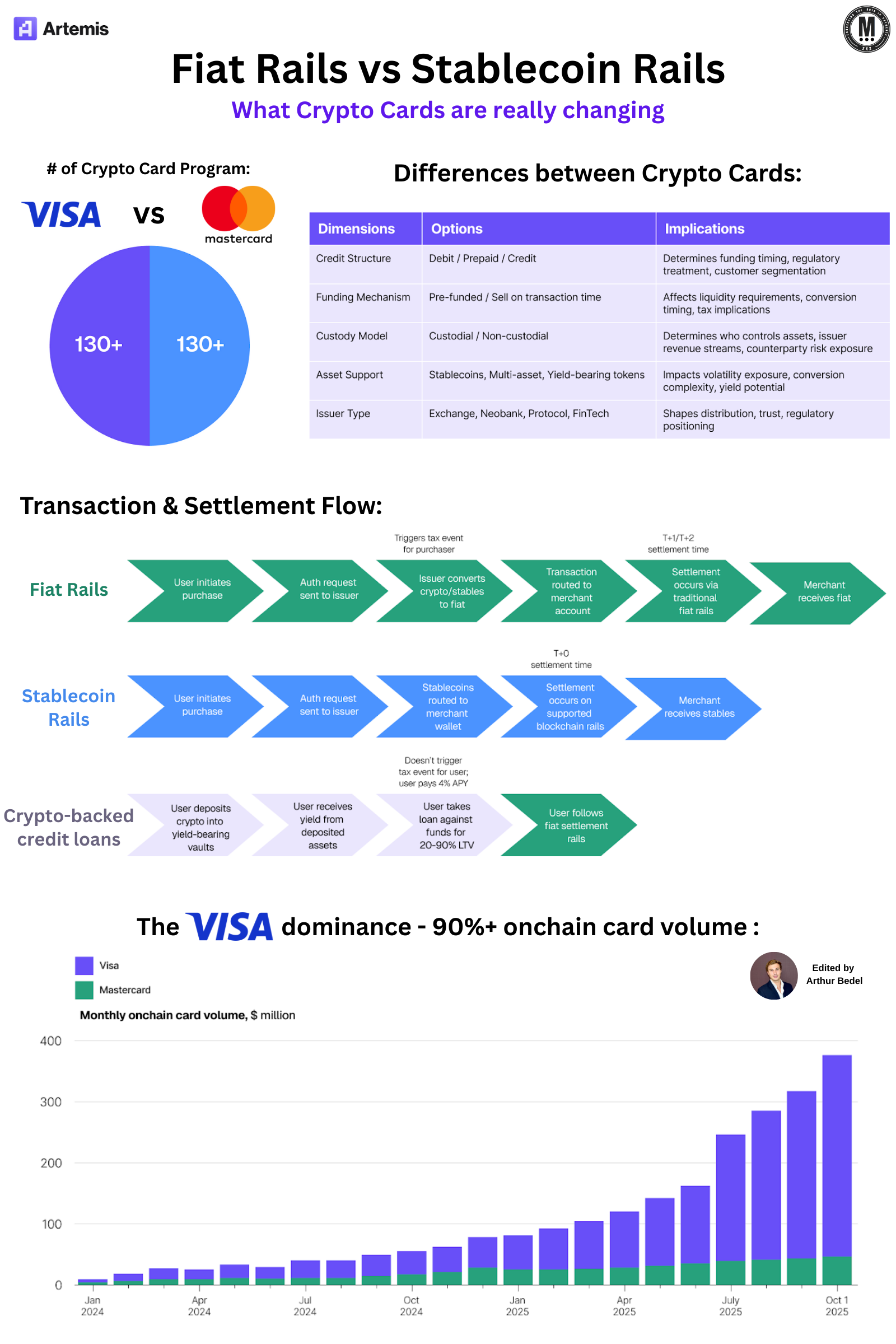

𝐅𝐢𝐚𝐭 𝐑𝐚𝐢𝐥𝐬 𝐯𝐬 𝐒𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧 𝐑𝐚𝐢𝐥𝐬 — 𝐰𝐡𝐚𝐭 𝐜𝐫𝐲𝐩𝐭𝐨 𝐜𝐚𝐫𝐝𝐬 𝐚𝐫𝐞 𝐫𝐞𝐚𝐥𝐥𝐲 𝐜𝐡𝐚𝐧𝐠𝐢𝐧𝐠 👇 Created by Arthur Bedel 💳 ♻️

At checkout, everything looks the same.

↳ Tap. Approve. Done.

But behind the scenes, the settlement path can be completely different... and that's what stablecoin/crypto cards are really changing:

→ Not the user experience...

↳ The 𝐫𝐚𝐢𝐥𝐬.

1️⃣ Most "crypto cards" still settle like traditional cards:

→ user pays

→ issuer converts assets to fiat

→ merchant receives fiat

→ settlement happens on fiat rails (T+1 / T+2)

So yes, it works globally. But it still inherits the classic constraints:

↳ timing, intermediaries, cost, and conversion friction.

2️⃣ Now compare that with 𝐬𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧 𝐬𝐞𝐭𝐭𝐥𝐞𝐦𝐞𝐧𝐭:

→ user pays

→ stablecoins are routed to a merchant wallet (i.e. Dfns)

→ settlement happens on supported blockchain rails

→ merchant receives stablecoins (often T+0)

= Same card swipe.

↳ Completely different settlement engine and once settlement becomes programmable, the implications get wild:

✔️ faster merchant access to funds

✔️ new treasury + liquidity models

✔️ real-time cross-border settlement

✔️ lower operational friction (reconciliation, prefunding, trapped cash)

✔️ stablecoins becoming a real global liquidity layer

This is also where the "modern stack" shows up: you need secure wallet infrastructure and policy controls to move value at scale. Platforms like Dfns are becoming critical infrastructure for #issuers and #fintechs to manage wallets, keys, permissions, and transaction governance behind these flows.

"𝐀𝐥𝐥 𝐜𝐚𝐫𝐝𝐬 𝐚𝐫𝐞 𝐧𝐨𝐭 𝐭𝐡𝐞 𝐬𝐚𝐦𝐞" → crypto cards" are not all built the same. The differences matter:

→ 𝐜𝐫𝐞𝐝𝐢𝐭 𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 (debit / prepaid / credit)

→ 𝐟𝐮𝐧𝐝𝐢𝐧𝐠 (prefunded vs sell-at-transaction-time)

→ 𝐜𝐮𝐬𝐭𝐨𝐝𝐲 (custodial vs non-custodial)

→ 𝐚𝐬𝐬𝐞𝐭 𝐬𝐮𝐩𝐩𝐨𝐫𝐭 (stablecoins vs multi-asset vs yield-bearing)

→ 𝐢𝐬𝐬𝐮𝐞𝐫 𝐭𝐲𝐩𝐞 (exchange, neobank, protocol, fintech)

In other words:

2 cards can look identical in a wallet...

↳ but behave completely differently in settlement, economics, and risk.

And on the merchant side, we're also seeing new models emerge — like Breeze — rethinking how merchants can accept and settle using stablecoin rails (and what "Merchant-Of-Record" can look like in a programmable world).

🚨 One stat in this infographic that jumped out:

↳ Visa now represents 𝐨𝐯𝐞𝐫 𝟗𝟎% of onchain card volume.

That's a big signal that stablecoin settlement through card distribution is scaling fast and that networks are taking this seriously.

↳

𝐌𝐲 𝐭𝐚𝐤𝐞:

1️⃣ Cards are still the best distribution layer in payments.

2️⃣ Stablecoins are becoming the best settlement layer.

3️⃣ Stablecoin / Crypto cards are simply the bridge between the two.

Source: Artemis

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()