Peru’s CBDC Just Passed 3.5 Million Users

Hey Payments Fanatic!

CBDCs often generate plenty of headlines but very little real-world usage.

Peru might be starting to change that.

The country's central bank has extended its retail CBDC pilot through March 2027 after the project surpassed 3.5 million users and recorded triple-digit growth in balances across some of Peru's least-banked regions.

What makes this interesting is where the adoption is happening.

Rather than targeting traditional banking customers, the pilot focuses on underserved regions where access to financial services remains limited.

To reach those users, the central bank partnered with telecom provider Bitel and distributed its digital currency through a mobile wallet called BiPay, effectively using mobile infrastructure instead of traditional banking rails.

More importantly, people appear to be using it. Balances in circulation have grown rapidly, suggesting the CBDC is becoming part of everyday financial activity rather than just another pilot project.

If successful, Peru could become one of the strongest examples yet of a CBDC solving a genuine financial inclusion problem rather than simply digitizing money for people who already have access to banking.

And if you keep scrolling, you'll also find our key takeaways from Money20/20 Europe, where AI, digital assets, and next-generation payments infrastructure dominated the conversation.

Today's remaining Payments headlines are just below. 👇 See you tomorrow!

Cheers,

INSIGHTS

📊 Busy at Money 20/20 and missed the headlines?

Same here, so I've made a full recap.

NEWS

🌍 Backbase collaborates with Mastercard to simplify cross-border payments for banks. The collaboration is designed to accelerate near real-time cross-border payment adoption among financial institutions worldwide, enabling them to deploy international payment solutions while reducing implementation complexity and time-to-market.

🇪🇬 Telda and Mastercard launch integrated payments and investment wallet in Egypt. This collaboration democratizes access to the capital market, empowering new customer segments without requiring advanced financial expertise and advancing Egypt’s vision for digital financial transformation.

🇨🇱 Pomelo obtained authorisation from Chile’s Financial Market Commission to operate as a non-bank issuer of prepaid cards. The license strengthens Pomelo’s infrastructure offering in the country, allowing FinTechs, digital wallets, and enterprises to launch prepaid card programs through a single platform while Pomelo manages regulatory compliance and operational requirements.

🇵🇪 Peru’s central bank extends digital currency pilot to 2027 after surpassing 3.5 million users. The initiative, delivered through the BiPay wallet in partnership with Bitel, has attracted more than 3.5 million users and is aimed at expanding financial inclusion by providing digital payments and transfers to populations with limited access to traditional banking services.

🇪🇬 Egyptian POS financing FinTech Blnk raises $37 million. With the new funding, the company will extend its tech capabilities, expand into new products, explore geographic expansion, and launch its credit card programme, enabling customers to utilise the credit limit beyond its network.

🇪🇸 Bankinter customers in Spain can now split their payments when making purchases with Apple Pay. This option offers a convenient and secure way to pay for a purchase. Customers can choose from monthly payment plans of between three and twelve months directly at the time of purchase.

🌏 Visa promotes Adeline Kim to a wider role across Southeast Asia. Kim will now oversee Visa’s business across the three Southeast Asian markets, while continuing to work with clients and partners across the region. Read more

🌍 Revolut is leveraging its Formula 1 partnership with Audi to strengthen its brand positioning and accelerate growth in payments and business banking. The FinTech is using the platform to promote services such as Revolut Business and Revolut Pay, while pursuing its ambition to become a leading European payments provider and compete more directly with players like PayPal, Stripe, and Adyen.

🇨🇳 Tencent is testing AI-powered payment capabilities through WeChat Pay, enabling AI agents to complete shopping transactions within conversational workflows. Initially piloted with WorkBuddy and QClaw, the solution allows users to authorize AI-driven purchases using dedicated payment cards with spending limits and user confirmation controls.

🇰🇭 Cambodia becomes the 9th country to accept UPI payments. Under this, Indian travellers can use their present UPI-enabled apps to make QR-code payments across the country. Continue reading

🇸🇬 WasabiCard completed its Series Pre-A funding round. The funding will be used to strengthen WasabiCard's global payment infrastructure, expand stablecoin-powered card and payout capabilities, accelerate international growth, and support continued investment in product development and compliance.

🇺🇸 MoonPay powers instant Apple Pay onboarding in Bread. The integration embeds payments, identity verification, and onboarding into a seamless native experience, supporting Bread’s vision of combining AI-driven banking with Bitcoin-based financial services.

🇺🇸 MNEE Pay announces Stripe integration to bring stablecoin payments to mainstream commerce. The integration supports USDC and USDT across multiple blockchains, allowing businesses to add stablecoin acceptance without changing their existing payment workflows.

🇺🇸 Nuvion joins Circle Payments Network. This integration expands Nuvion's ability to offer instant, secure, multi-currency settlement across markets, deepening its mission to make global finance accessible to everyone, from creators earning across borders, businesses expanding internationally, to large marketplaces and global platforms running high-volume payment flows.

🇯🇵 PayPay to buy a majority stake in T&D Financial Life. Through the addition of life insurance, PayPay intends to extend its financial services across different stages of customers’ lives, including daily payments, insurance and asset management.

GOLDEN NUGGET

𝐌𝐨𝐬𝐭 F𝐢𝐧T𝐞𝐜𝐡𝐬 𝐝𝐨𝐧'𝐭 𝐡𝐚𝐯𝐞 𝐚 𝐫𝐞𝐜𝐨𝐧𝐜𝐢𝐥𝐢𝐚𝐭𝐢𝐨𝐧 𝐩𝐫𝐨𝐛𝐥𝐞𝐦. 𝐓𝐡𝐞𝐲 𝐡𝐚𝐯𝐞 𝐚 𝐭𝐫𝐮𝐭𝐡 𝐩𝐫𝐨𝐛𝐥𝐞𝐦. 👇Created by Arthur Bedel 💳 ♻️

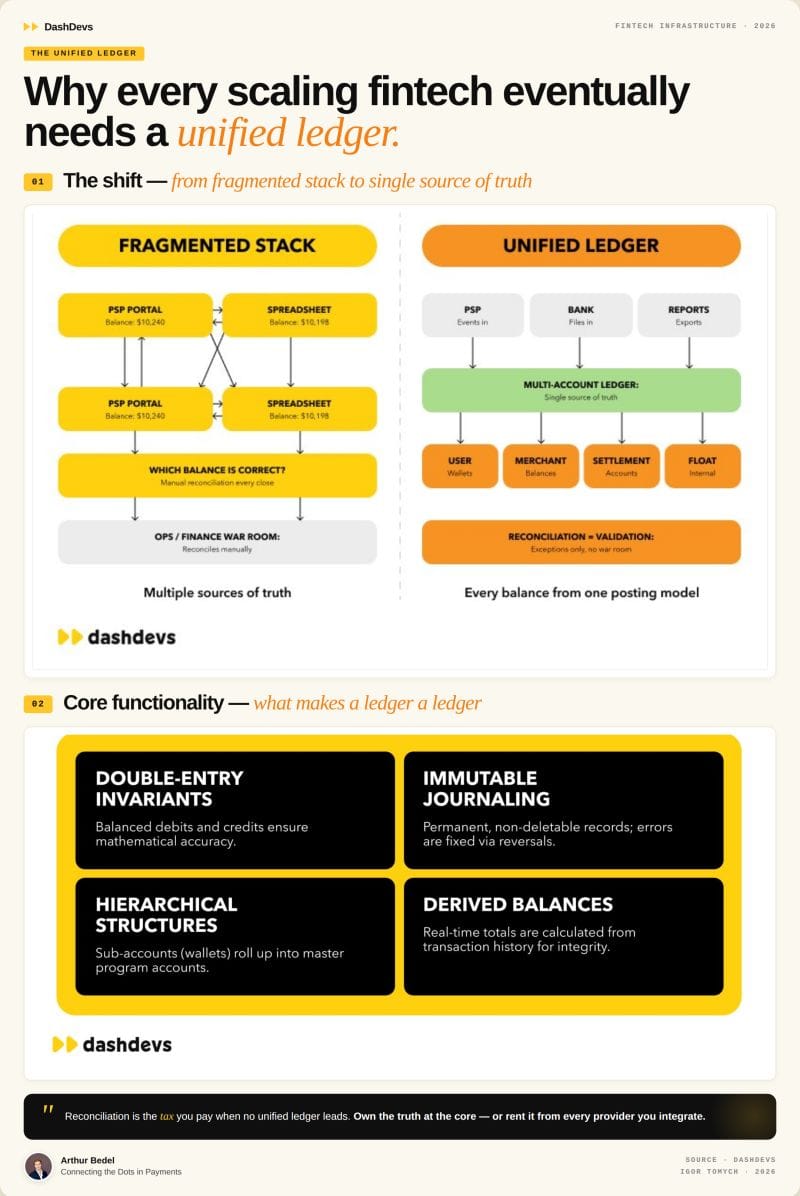

Every scaling FinTech eventually hits the same wall.

The PSP says the balance is $10,240. The spreadsheet says $10,198. The core system says something else entirely. Three numbers. One customer. Nobody can sign off on which one is right.

That is not a tooling problem. It is an architecture problem.

→ Customer support sees one balance

→ Finance exports another

→ Risk tracks a third

→ Every close becomes a war room

→ Every new PSP adds its own mini-ledger

→ Every new market multiplies the chaos

The root cause is always the same. There is no unified ledger at the core.

𝐖𝐡𝐲 𝐭𝐡𝐢𝐬 𝐤𝐞𝐞𝐩𝐬 𝐡𝐚𝐩𝐩𝐞𝐧𝐢𝐧𝐠

In early-stage builds, the transaction ledger is implicit. You store events in an app database. You mirror a provider's idempotency keys. You hope you can recompute a balance if anyone ever asks.

That works until the product surface branches. Wallets. Treasury accounts. Marketplace payouts. Fees. Reserves. Compliance holds. Each one needs a slightly different view of the same money.

Without a single source of truth, you don't get one. You get a truce that lasts until the next chargeback or duplicate webhook breaks it.

𝐖𝐡𝐚𝐭 𝐚 𝐮𝐧𝐢𝐟𝐢𝐞𝐝 𝐥𝐞𝐝𝐠𝐞𝐫 𝐜𝐡𝐚𝐧𝐠𝐞𝐬

→ PSPs, banks, and reports feed in. They don't own truth anymore

→ User, merchant, settlement, and float balances all derive from one posting model

→ Reconciliation becomes validation, not investigation

→ New products and rails plug in without re-platforming

→ Audit trails are queryable, not reconstructed in a two-week sprint

𝐇𝐨𝐰 𝐦𝐨𝐧𝐞𝐲 𝐚𝐜𝐭𝐮𝐚𝐥𝐥𝐲 𝐦𝐨𝐯𝐞𝐬 𝐭𝐡𝐫𝐨𝐮𝐠𝐡 𝐢𝐭

1. Authorization. Hold placed.

2. Capture. Fee deducted.

3. Clearing. Network settles.

4. Settlement. Money transferred.

5. Complete. Merchant paid.

With an optional dispute or reversal path that posts as a linked reversal. Not a mystery row in a different system.

Real-time rails removed the buffer. Multi-product platforms removed the simplicity. Sponsor banks and regulators are asking harder questions than they were two years ago.

FinTechs that scale without a re-architecture in year three tend to invest in the ledger early. When the product is small enough that the cost is contained. The ones that don't pay it back later with interest, during a funding round or an audit.

Reconciliation is the tax you pay when no unified ledger leads.

Source: DashDevs LLC ·Igor Tomych

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()