VaulFi and Noah Launch First Direct-to-Bank Stablecoin Bridge for North Africa

Hey Payments Fanatic!

VaulFi, the stablecoin-powered neobank, and Noah, the global payments infrastructure provider, are partnering to eliminate the "Triple Extraction Problem" in North Africa.

This problem represents a combination of high commissions, predatory FX rates, and a widening 80% gap between official and parallel currency markets.

With the VaulFi and Noah partnership, African freelancers and businesses can now receive international payments in under two hours, bypassing the legacy 21-day SWIFT settlement cycle.

"Birthplace should not determine your economic potential," said Shah Ramezani, Founder and CEO of Noah. "We are making the complex plumbing of cross-border finance invisible so that the modern North African workforce can finally be paid what they are truly worth, in real-time."

This shift is particularly critical for the region's growing class of remote workers and expats. By localizing international financial services and accepting local documentation for KYC, VaulFi and Noah are ensuring that the 24/7 liquidity of the digital asset world is accessible to everyone.

The payments news keeps coming below 👇 Back tomorrow!

Cheers,

INSIGHTS

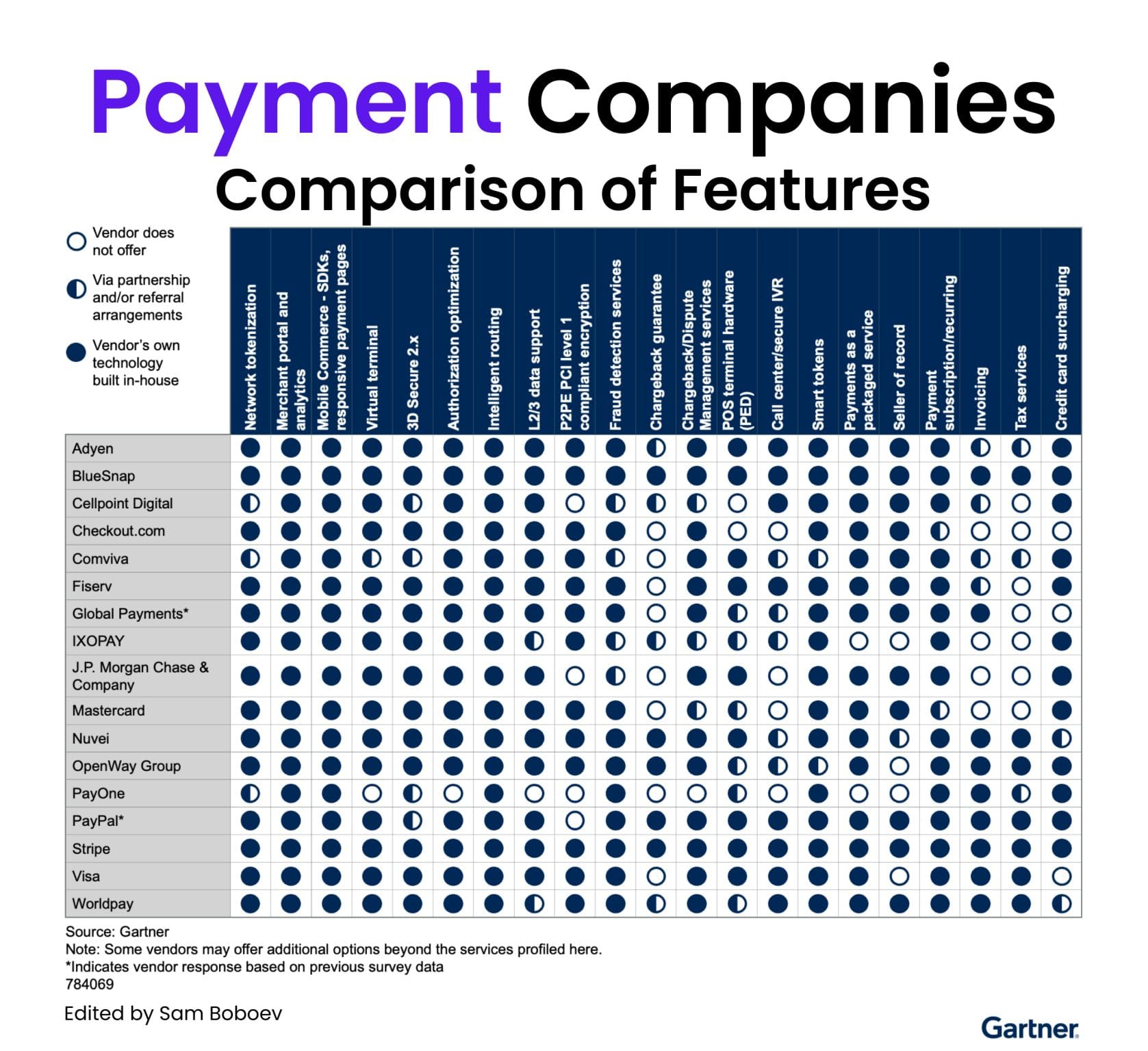

Digital Commerce Payment Platforms 👇

NEWS

🌎 VaulFi and Noah launch first direct-to-bank stablecoin bridge for North Africa. The partnership leverages Noah’s regulated settlement engine to provide VaulFi users with dedicated virtual bank accounts. The collaboration replaces slow, costly traditional transfers with real-time settlement into digital euros and dollars.

🇩🇪 DashDevs took the stage at Merchant Payments Ecosystem 2026 in Berlin, where CEO Igor Tomych joined a panel on open banking and interoperability. The session explored regulation, AI’s impact on finance, and the challenges of achieving seamless data exchange across financial ecosystems.

🇷🇺 Visa is applying for trademark registration in the Russian Federation. Visa filed trademark applications in Russia to protect its brand and technologies, but a return to the market remains unlikely in the near term due to ongoing U.S. sanctions and regulatory barriers.

🇺🇸 Visa and payment firms warned by US regulator on debanking concern. The move comes amid growing scrutiny over “debanking” practices and concerns about access to financial services. Read more

🌏 Cambodia and Singapore complete full interoperability of cross-border QR payment linkage. The service allows users to view transparent foreign exchange rates before confirming payment, ensuring clarity and confidence in every transaction. Payments are completed instantly without the need for cash exchange.

🇬🇧 Maven North East Strengthens Support for FinTech Specialist, Kani. The transaction will enable Kani to invest in new product development to prepare for upcoming regulations requiring firms to provide audit-ready reconciliation of client funds across the UK and global payments markets.

🇦🇺 EML Payments appoints Adam Olding as Global CEO. With over 25 years of experience in payments, financial services, and corporate governance, Olding brings a wealth of expertise to the position. In his new capacity, Olding will assume responsibility for day-to-day management and lead the executive leadership team in executing the company's growth priorities.

🇺🇸 Wirex and Crossmint announce card integration to connect stablecoin wallets and real-world spending. The two companies have directly connected Crossmint's smart wallet and stablecoin orchestration infrastructure with Wirex's card issuance platform, giving FinTechs a single connected stack that takes users from stablecoin balance to real-world spending.

🇵🇱 SIBS has completed the acquisition of ITCARD after obtaining all the necessary regulatory approvals in Poland. The operation will allow SIBS to strengthen its omnichannel solutions offering, combining expertise across the entire payments value chain and consolidate its position as one of the leading international players in the sector.

🇷🇺 Russia orders mobile operators to disable Apple account payments to limit VPN access. The measure is intended to limit Russians’ ability to pay for VPN services, which are widely used to bypass internet restrictions. Continue reading

🇬🇧 PayPoint splits its business into four independent units, with clearly defined operating structures, a greater focus on growth opportunities, and a more accountable operating culture. This will enable a more focused portfolio of businesses and better harness the Group’s collective capabilities.

🇺🇸 Nino Galluzzo has joined Tempo as Creative Director. Galluzzo has joined Tempo to lead creative and brand, marking a new chapter as the Stripe- and Paradigm-incubated company builds out its vision and identity.

🇧🇷 Brazilian company BTG suffers an attempted hacker attack and suspends operations with Pix. BTG said in a statement that it identified unusual activity related to Pix on Sunday morning. The bank clarifies that there was no access to customer accounts and that account holders’ data was not exposed.

🇬🇧 Wise launches UK current account to take on high street banks. Designed for people with international needs, the new current account comes with a Travel Hub. It includes a new Airport Lounge Pass feature to make international travel more convenient. Customers in the UK and other select markets can now purchase a one-off lounge access pass in a few clicks within their Wise app.

🇺🇸 Plaid CFO, Seun Sodipo, says FinTech company has earned the right to ‘pick our time’ for IPO. As IPO preparations continue, Sodipo is focused on growth, and the FinTech company is seeing results: Annual recurring revenue last year climbed 40% from the year earlier, to more than $500 million, according to Plaid.

GOLDEN NUGGET

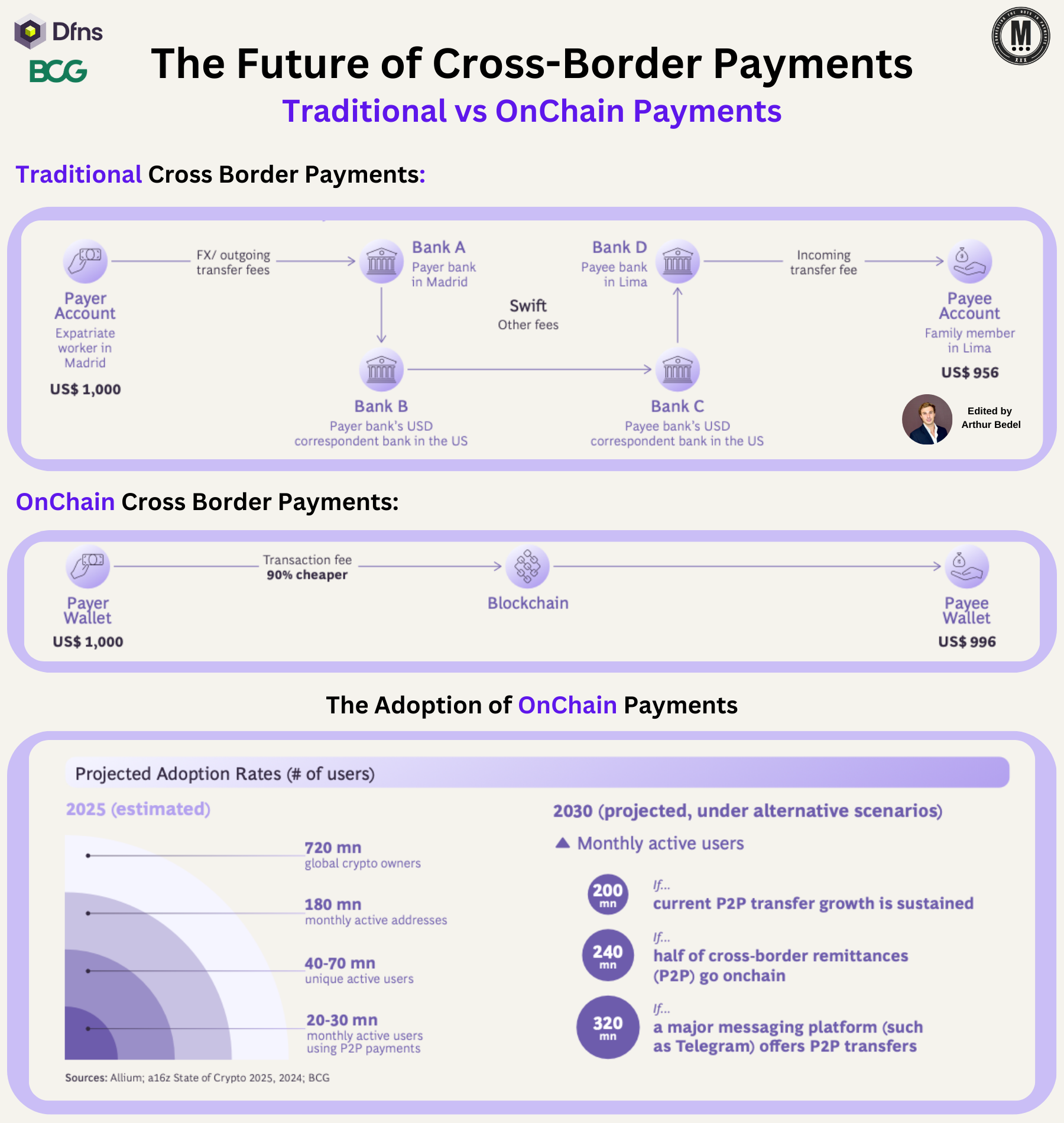

𝐓𝐡𝐞 𝐅𝐮𝐭𝐮𝐫𝐞 𝐨𝐟 𝐂𝐫𝐨𝐬𝐬-𝐁𝐨𝐫𝐝𝐞𝐫 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 — Traditional vs OnChain Payments👇Created by Arthur Bedel 💳 ♻️

For decades, moving money across borders meant navigating a maze: correspondent banks, cut-off times, FX spreads, SWIFT messages, reconciliation layers... and fees eating away at value.

That model worked for the era of batch banking. It doesn't work for the era of real-time digital commerce.

↳

𝐖𝐡𝐚𝐭 𝐭𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐜𝐫𝐨𝐬𝐬-𝐛𝐨𝐫𝐝𝐞𝐫 𝐚𝐜𝐭𝐮𝐚𝐥𝐥𝐲 𝐥𝐨𝐨𝐤𝐬 𝐥𝐢𝐤𝐞:

A $1,000 transfer can pass through:

• Payer bank

• USD correspondent bank

• Payee correspondent bank

• Payee bank

Each hop = fees + time + opacity.

Result → ~$956 arrives days later.

This isn't a UX problem.

It's an infrastructure problem.

↳

𝐖𝐡𝐚𝐭 𝐎𝐧𝐂𝐡𝐚𝐢𝐧 𝐜𝐡𝐚𝐧𝐠𝐞𝐬:

Instead of messaging layers between banks, value moves directly wallet → wallet on a shared ledger.

• Settlement in seconds

• ~90% lower transaction cost

• Full traceability

• 24/7 availability

• No correspondent chain

Same $1,000 → ~$996 received.

Platforms like Breeze are already turning this into real payment flows, embedding OnChain rails into Merchant-Of-Record (#MOR) and payouts so businesses can settle globally without touching legacy correspondent rails.

That's not incremental improvement.

That's a different operating system.

↳

𝐖𝐡𝐲 𝐜𝐫𝐨𝐬𝐬-𝐛𝐨𝐫𝐝𝐞𝐫 𝐢𝐬 𝐭𝐡𝐞 𝐛𝐞𝐬𝐭 𝐮𝐬𝐞 𝐜𝐚𝐬𝐞 𝐟𝐨𝐫 𝐬𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧 𝐫𝐚𝐢𝐥𝐬 👇

Because the pain is structural:

• Fragmented liquidity

• Multi-day settlement

• FX friction

• Limited operating hours

• Heavy reconciliation

OnChain collapses those layers into one atomic transaction. The payment becomes data + value moving together.

↳

𝐁𝐮𝐭 𝐭𝐡𝐢𝐬 𝐨𝐧𝐥𝐲 𝐰𝐨𝐫𝐤𝐬 𝐰𝐢𝐭𝐡 𝐭𝐡𝐞 𝐫𝐢𝐠𝐡𝐭 𝐰𝐚𝐥𝐥𝐞𝐭 𝐢𝐧𝐟𝐫𝐚

Institutions don't need "more crypto tools." They need bank-grade operating rails for digital assets:

• Policy-driven transaction governance

• MPC/HSM key management

• Compliance & identity controls

• Workflow approvals

• Secure bridging between TradFi & OnChain

That's where Dfns fits — providing the wallet infrastructure layer that lets #Banks, #PSPs, and #FinTechs run OnChain payments.

Not DeFi vs TradFi.

→ 𝐓𝐫𝐚𝐝𝐅𝐢 𝐨𝐧 𝐧𝐞𝐰 𝐫𝐚𝐢𝐥𝐬.

↳

𝐖𝐡𝐚𝐭 𝐭𝐡𝐞 𝐧𝐞𝐱𝐭 𝟓 𝐲𝐞𝐚𝐫𝐬 𝐥𝐨𝐨𝐤 𝐥𝐢𝐤𝐞

• Wallet-to-wallet remittances embedded in banking apps

• Treasury moving liquidity OnChain between entities

• PSPs settling payouts in minutes instead of days

• FX happening at protocol level

• Stablecoin rails powering B2B flows

We won't call this "blockchain payments."

We'll just call it... payments.

↳

The future of cross-border isn't another messaging standard. It's a new infrastructure.

🚨 What cross-border flow would you move OnChain first — remittances, payouts, or treasury?

Source: Dfns & Boston Consulting Group (BCG)

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()