Wero Takes Another Step Toward Becoming Europe’s Payment Network

Hey Payments Fanatic!

Europe's push for payment sovereignty just picked up another important win.

BoursoBank, France's largest online bank with nearly 9 million customers, plans to integrate Wero by the end of 2026, bringing the European payment solution to millions of additional users.

At first glance, this might look like just another P2P payment rollout.

I think it's much bigger than that.

For years, European payments have relied heavily on international card schemes and global technology platforms. Wero is one of the first serious attempts to build a unified European alternative that operates across multiple countries on top of instant account-to-account payments.

What stood out to me is how quickly adoption is building. Wero already has more than 55 million users, with France becoming one of its strongest markets.

BoursoBank will even make the service available to customers aged 10 to 17, a sign that banks increasingly see instant account-to-account payments as a mainstream behavior rather than a niche feature.

And if you keep scrolling, you'll also find a practical whitepaper from Ecommpay on the fraud threats merchants are facing today and what they're doing to stay ahead of them.

Today's remaining Payments headlines are just below. 👇 See you tomorrow!

Cheers,

INSIGHTS

📰 Fraud is evolving. Is your defence keeping up? By Ecommpay. The research highlights the growing cost of e-commerce fraud, with UK payment fraud losses reaching £1.17 billion in 2024. The guide identifies nine major threats and provides practical strategies to help merchants reduce chargebacks, protect revenue, and strengthen fraud prevention without adding friction to the customer experience. Read the full guide here

NEWS

🌍 Mastercard launches Agent Pay for Machines, enabling AI agents to execute secure, programmable payments at machine speed. Backed by partners including Stripe, Coinbase, Checkout.com, and Getnet, the platform is designed to support the next wave of agentic commerce and machine-to-machine transactions.

🌍 Airwallex has officially launched Airwallex Billing, a new solution designed to help businesses manage increasingly complex and dynamic pricing models, including AI-driven and usage-based billing. The release is part of a broader product update that also includes expanded local payment acceptance capabilities, enhanced spend management tools, and new infrastructure features.

🇫🇷 BoursoBank integrates Wero into its payment solutions. This new free feature complements BoursoBank’s fee-free offering for transfers and payments, including foreign currency and international transactions. Through this partnership, BoursoBank is contributing to the emergence of a credible European solution for everyday payments.

🇲🇽 Clip partners with Ant on a consumer payments wallet in Mexico. Clip said the platform will help consumers and merchants shift from cash to digital payments through a mobile app that supports multiple payment methods, including bank cards, digital wallets, and instant payments.

🇵🇱 Polish FinTech paymove secures €2.12 million to drive European expansion. The company plans to expand across Western Europe and develop infrastructure for AI-agent payments, advancing its vision of a Payment-as-a-Service platform spanning e-commerce, offline payments, and agentic commerce.

🇮🇳 Cashfree Payments unlocks India for the world; the cross-border suite is now live across 40 countries. Cashfree Payments can now enable global businesses in e-commerce, SaaS, travel, and digital goods seeking to access India's fast-growing consumer base.

🇺🇸 Volante launches “Vol360i” Agentic AI at the core of payments. The core upgrade unlocks autonomous and semi-autonomous collaboration to reduce manual intervention, significantly increasing straight-through processing (STP) rates to over 95%, accelerating exception resolution, and proactively managing SLA performance.

🇬🇧 Stripe has introduced new capabilities for UK businesses, including multi-currency treasury accounts, AI-commerce integrations, enhanced fraud protection, and global payment tools. The updates enable companies to manage GBP, EUR, and USD balances, expand sales to 195 countries, and optimize cross-border conversions.

🇸🇬 Ant International considers raising $1 billion to boost growth. The raise could value the business at more than $10 billion, with existing investors including General Atlantic and Silver Lake said to be among those approached as Ant International expands its global payments and digital finance operations.

🇺🇸 Moment and Ramp partner to bring institutional cash management to finance teams. The collaboration enables businesses to access professionally managed fixed-income portfolios, automated cash optimization, and treasury workflows.

🇵🇭 Munify integrates with Circle Payments Network to enable USDC-powered local payouts in the Philippines. Through the integration, Munify enables users to receive funds globally in USDC and convert them into Philippine pesos for payout to local bank accounts and digital wallets.

🌎 Adyen has promoted Shepherd Smith to President of North America. Smith will lead the company’s regional growth efforts while maintaining Adyen’s existing strategy of helping merchants scale through unified payments and financial technology solutions.

GOLDEN NUGGET

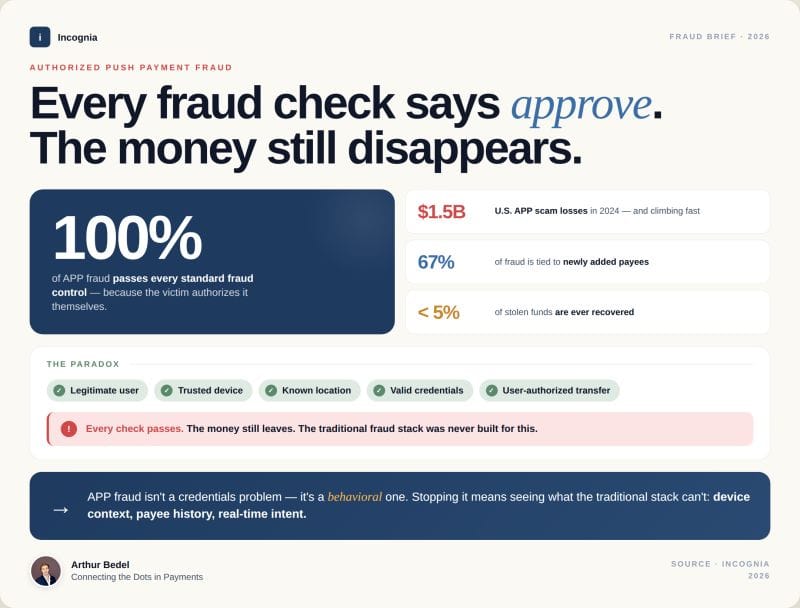

𝐀𝐮𝐭𝐡𝐨𝐫𝐢𝐳𝐞𝐝 𝐏𝐮𝐬𝐡 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐅𝐫𝐚𝐮𝐝, every fraud check approved and still the money disappears.👇Created by Arthur Bedel 💳 ♻️

100% of it passes every standard fraud control. Not 80%. Not 95%. All of it.

Why? Because the victim authorizes the transfer themselves.

→ Legitimate user

→ Trusted device

→ Known location

→ Valid credentials

→ User-authorized transfer

Every box ticked. Every signal green. Money gone.

𝐇𝐨𝐰 𝐰𝐞 𝐠𝐨𝐭 𝐡𝐞𝐫𝐞:

Real-time rails removed the safety net. Generative AI removed the cost of impersonation. A scammer with a cloned voice and a phone now does what an organized fraud ring used to need.

The fraudster never touches the device. They just keep the victim on the line.

𝐓𝐡𝐞 𝐧𝐮𝐦𝐛𝐞𝐫𝐬

→ $1.5B in U.S. APP scam losses in 2024 — and climbing fast

→ 67% of fraud tied to newly added payees

→ Less than 5% of stolen funds ever recovered

𝐖𝐡𝐞𝐫𝐞 𝐝𝐞𝐭𝐞𝐜𝐭𝐢𝐨𝐧 𝐡𝐚𝐬 𝐭𝐨 𝐦𝐨𝐯𝐞

The credentials are valid. The device is real. The user pressed send. None of that is the signal anymore.

→ Active call detection — a device on a live call while adding a new payee is the highest-confidence scam signal in fraud today

→ First-time payee scrutiny — friction beats refunds

→ Shared mule intelligence across institutions — the money has to land somewhere

→ Behavioral anomalies — large amount, new payee, active call = textbook fingerprint

APP fraud isn't a credentials problem. It's a behavioral one.

Stopping it means seeing what the traditional stack can't — device context, payee history, real-time intent.

Banks that adapt protect their customers. The rest keep reimbursing them.

So who should carry the liability when the customer authorized the transfer themselves — the bank, the rail, or the user? Drop your take.

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()