Worldline Sells India Payments Arm to BillDesk for ~€60M

Hey Payments Fanatic!

Worldline is selling its Indian payment activities to BillDesk for an estimated equity value of around €60M.

This is part of its broader strategy to refocus on core European payment operations. Important nuance: this isn’t a full exit from the ecosystem.

Worldline will enter into a long-term technology and software agreement with BillDesk. The Indian business changes hands. The software layer stays connected.

For reference: ~€90M revenue impact; ~€8M adjusted EBITDA; Free cash flow broadly neutral; ~Combined disposal proceeds across recent sales now estimated at €540–590M.

The message is clear…

Worldline is narrowing its scope, strengthening its balance sheet, and concentrating capital on Europe.

India remains a talent and innovation hub through its Global Competence Centres. But operational ownership of payments is moving to a domestic champion with local scale.

Less geographic spread. More strategic focus. In payments, sometimes discipline is the growth story.

Scroll down to see what else is moving in Payments today 👇I'll be back tomorrow with more stories from the sector.

Cheers,

INSIGHTS

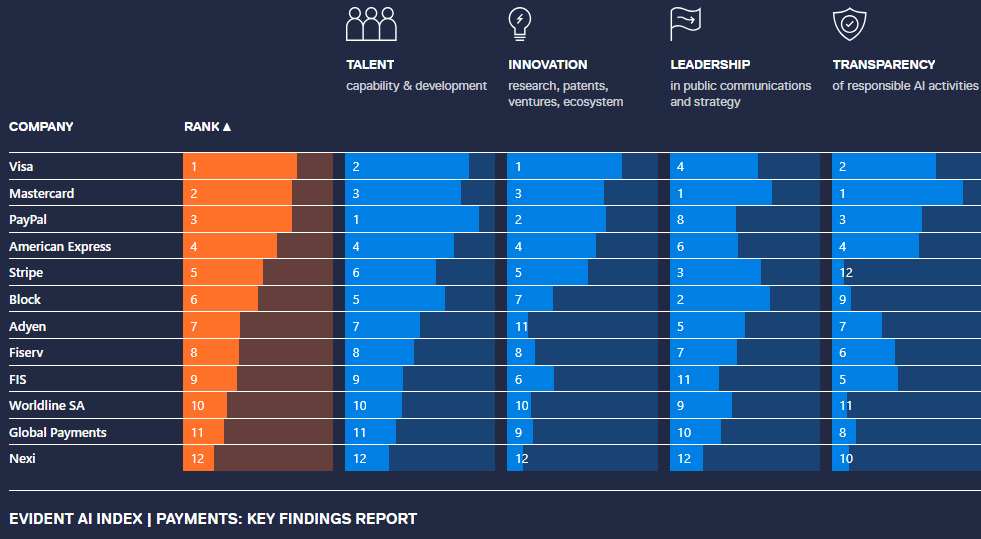

📊 EVIDENT AI INDEX | PAYMENTS: Benchmarking the AI maturity of the largest payment networks and processors in North America and Europe. It evaluates four key pillars: talent, innovation, leadership, and transparency, offering a comprehensive view of who is leading in AI and how the payments sector is evolving.

NEWS

🇺🇸 Mastercard is staffing up for stablecoins and DeFi. The Director of Crypto Flows will lead stablecoin-linked card launches, expand DeFi and blockchain payment integrations, and update Mastercard’s network rules and risk systems to support Web3 transactions.

🇮🇳 Worldline announces strategic sale of its Indian payment activities to BillDesk. The transaction supports Worldline’s strategy to refocus on core European payment activities, strengthen its financial position, and redeploy capital. The group also remains committed to India as a strategic talent and innovation hub, particularly in automation and AI.

🇸🇬 SG FinTech startup Lyte raises $4.2m. By enabling payouts as fast as one business day, Lyte significantly reduces financial stress for sales professionals waiting on delayed commissions. The fresh capital will fuel product enhancements, AI integrations, and expansion into new markets like Australia.

🇺🇸 Verdict expected soon in Klarna’s $8.3 billion antitrust lawsuit against Google. The claim arises from Google’s abuse of dominance in online comparison shopping, as established by the European Commission in a binding 2017 decision and upheld without reservation by the Court of Justice of the European Union in September 2024.

🇺🇸 Klarna reaches 55 million monthly app users as usage surges 53% year over year. CEO Sebastian Siemiatkowski said the growth reflects Klarna’s shift toward becoming a global digital bank for everyday money management. Recent launches are driving increased daily usage and positioning the app as a central hub for consumer finances.

🌎 Oobit enables instant stablecoin transfers to bank accounts worldwide. Oobit has enabled wallet users to send stablecoins directly to bank accounts worldwide with near-instant settlement. The service removes traditional delays and intermediaries, allowing funds to be received without relying on SWIFT processing.

🇨🇦 Peoples Group teams with Fiserv to build Canada's next-generation payments platform. This leading technology will enable clients and partners to leverage instant payments, always-on infrastructure, and rich ISO 20022 data through direct connections to Canada's prominent payment systems, streamlining automation and enhancing digital client experiences.

🇺🇸 Slash announces collaboration with Visa DPS to power scalable, reliable card issuing platform. As part of its collaboration with Visa, the move gives Slash customers stronger controls and clearer data, with the capacity to scale alongside expanding transaction volume.

🇺🇸 Circle reports fourth quarter and full fiscal year 2025 financial results. Jeremy Allaire, Co-Founder, Chief Executive Officer, and Chairman at Circle, highlighted expanding USDC adoption across enterprises and public institutions, progress toward launching Arc mainnet, growth in CPN transaction volume, and rising momentum for EURC and USYC.

🌍 SumUp signs with Form3 for real-time payments across Europe. This expanded partnership will consolidate multiple payment capabilities through a single provider, simplifying SumUp’s payments infrastructure, reducing operational complexity, and enabling merchants to unlock growth across markets.

🇺🇸 Array acquires EarnUp to expand flexible, paycheck-aligned payment solutions. The acquisition brings EarnUp’s proven payment infrastructure and enterprise relationships into Array’s growing portfolio of embedded financial tools, expanding Array’s ability to support consumers navigating complex debt and cash-flow challenges.

🇺🇸 Xero has rolled out an online bill payments feature that combines the Xero platform with Melio’s payment processing capabilities. The online bill payments feature was designed to help small businesses turn bill payments from a constant headache into a more predictable, manageable part of running the business.

🇧🇷 Brazil’s Banco Braza brings real-backed BBRL stablecoin to Polygon. With this step, BBRL is no longer confined to a single blockchain setup and can now be used on Polygon for transfers and other on-chain transactions. The move to Polygon enables faster and lower-cost transactions, particularly for cross-border payments and business use cases.

🇺🇸 PLDT seeks US and Philippine listings for FinTech unit Maya. Maya’s foreign shareholders want the payment platform and digital bank operator to be listed in the US, PLDT Chairman and Chief Executive Officer Manuel Pangilinan said. “But we’re insisting on dual listing, here on PSE,” he added, referring to the Philippine Stock Exchange.

GOLDEN NUGGET

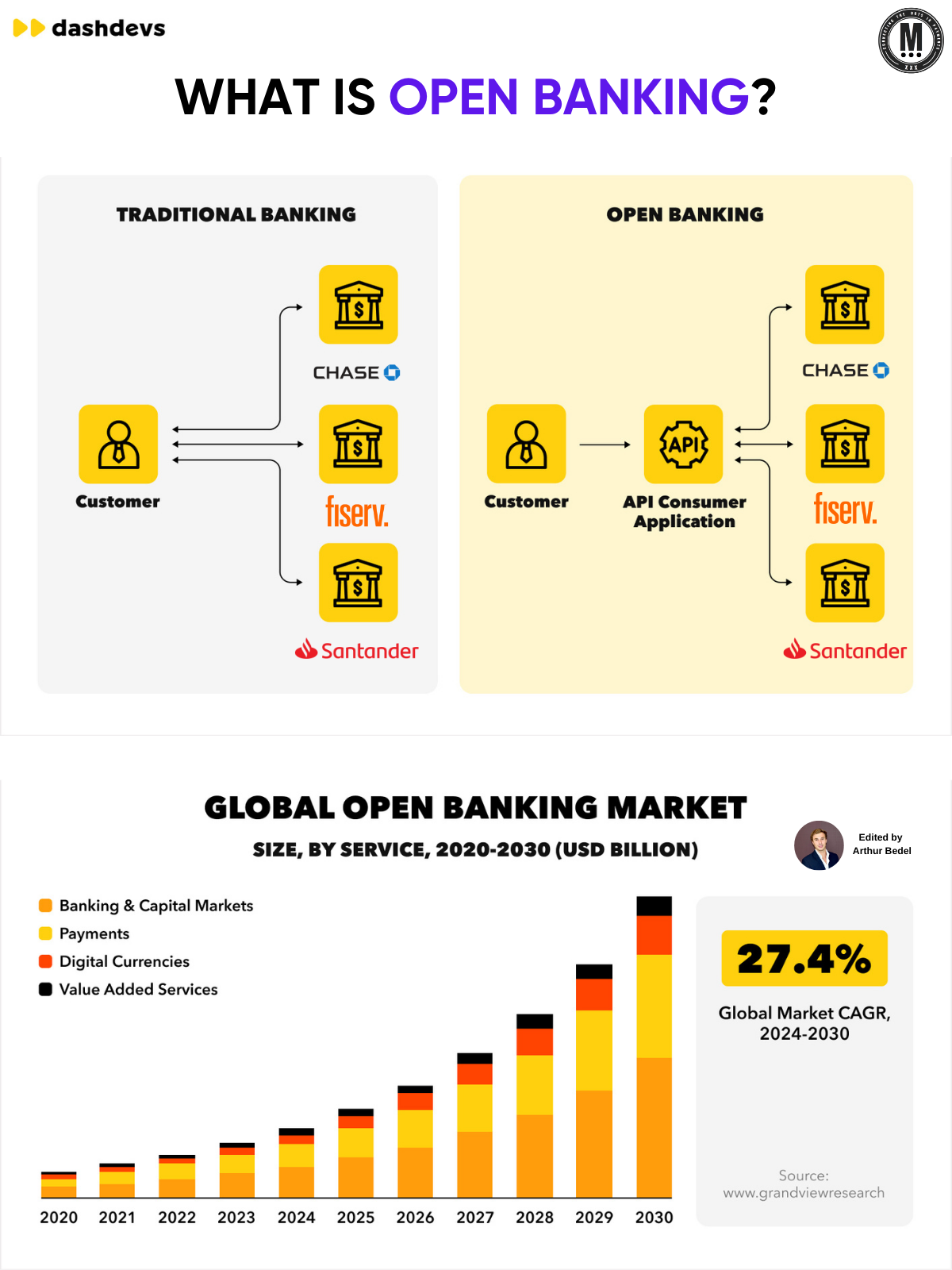

𝐖𝐡𝐚𝐭 𝐢𝐬 𝐎𝐩𝐞𝐧 𝐁𝐚𝐧𝐤𝐢𝐧𝐠 — 𝐚 𝐧𝐞𝐰 𝐢𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐥𝐚𝐲𝐞𝐫 𝐟𝐨𝐫 𝐩𝐚𝐲𝐦𝐞𝐧𝐭𝐬 👇Created by Arthur Bedel 💳 ♻️

Open Banking is not a product and not a new type of bank. It’s an API-based data and payment layer that allows customers — individuals or businesses — to securely share their bank data with third-party applications, only with explicit consent.

Instead of financial data being locked inside one institution, it becomes portable, permissioned, and usable in real time.

That shift is already changing how merchants handle payments, onboarding, and risk.

𝐓𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐁𝐚𝐧𝐤𝐢𝐧𝐠 𝐯𝐬 𝐎𝐩𝐞𝐧 𝐁𝐚𝐧𝐤𝐢𝐧𝐠

In traditional banking:

→ Customers interact directly with each bank

→ Data sits in silos

→ Every new service requires a new integration

With Open Banking:

→ Customers authorize access once

→ APIs connect banks to fintech and merchant apps

→ Data and payments move securely between systems

𝐇𝐨𝐰 𝐦𝐞𝐫𝐜𝐡𝐚𝐧𝐭𝐬 𝐮𝐬𝐞 𝐎𝐩𝐞𝐧 𝐁𝐚𝐧𝐤𝐢𝐧𝐠 𝐭𝐨𝐝𝐚𝐲

• Direct bank payments at checkout

Merchants like Zalando and Ryanair enable account-to-account payments by connecting directly to banks such as ING, Santander, or BNP Paribas, reducing card fees, fraud exposure, and chargebacks.

• Faster onboarding and credit decisions

Platforms and marketplaces use live bank data from institutions like Barclays or HSBC to verify income, cash flow, and business activity — removing manual document uploads and accelerating approvals.

• Real-time reconciliation and treasury visibility

Large merchants and PSPs pull transaction and balance data directly from banks like JPMorganChase or Deutsche Bank to automate reconciliation, improve cash-flow forecasting, and reduce operational overhead.

𝐓𝐡𝐞 𝐛𝐢𝐠𝐠𝐞𝐫 𝐩𝐢𝐜𝐭𝐮𝐫𝐞:

Open Banking laid the groundwork for:

→ Open Finance

→ Embedded finance

→ Real-time payments

→ Programmable money flows

The global Open Banking market is growing fast — with payments, value-added services, and data-driven products leading the expansion. A ~27% CAGR through 2030 isn’t hype; it reflects real adoption across banks, PSPs, and fintechs (DashDevs LLC)

Open Banking didn’t replace banks.

It opened the data layer — and merchants are already building on it.

Source: DashDevs LLC

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()