IRIS Joins Europe's Instant Payments Network

Hey Payments Fanatic!

Europe is taking another step toward making instant payments work across borders.

Greece's IRIS payment system now lets users send money instantly to people in Spain, Portugal, Italy, and Andorra using nothing more than a mobile phone number. No IBAN required.

It's another example of how Europe's domestic payment schemes are gradually becoming a single connected network rather than separate national systems. The goal isn't simply faster transfers. It's making cross-border payments feel as simple as sending money to someone in your own country.

There's plenty more waiting below.

You'll also find a fascinating conversation with Graham Robinson, CEO of CompoSecure, on why physical payment cards still matter in a digital world, plus a breakdown of Wise's latest FY26 results and what they reveal about the company's evolution beyond cross-border payments.

See what else is shaping Payments. 👇 See you tomorrow!

Cheers,

Marcel

Q&A

📰 Q&A: The Future of Payments Is Physical and Digital: A Conversation with Graham Robinson, President and CEO of Composecure. Robinson discusses why physical payment cards remain relevant, how metal cards strengthen customer engagement, and how blending digital and physical experiences is reshaping payments. Read the full Q&A here

NEWS

🌍 Cedar and Noah connect emerging market capital to global trade infrastructure. Cedar will provide regulated onboarding and compliance, while Noah delivers stablecoin-powered payment infrastructure, enabling faster, compliant, and more efficient international settlements.

🇬🇷 Greece’s IRIS Payments System expands to cross-border transfers in Europe. The new function applies only to person-to-person transfers between individuals. It allows users to send money to registered users of participating European payment services without entering an IBAN.

🇺🇸 Klarna submits application for U.S. banking license. If approved, Klarna Bank USA would be a wholly owned subsidiary of Klarna Inc., chartered in Utah and insured by the FDIC, with its own independent board, governance, and internal controls.

🌎 Google is rolling out a unified transaction history in Google Wallet, allowing users to view tap-to-pay purchases made on both Android phones and Wear OS smartwatches in a single timeline. The update provides a more complete view of spending across devices.

🌍 Adyen provides payment solutions to Xiaomi. By managing online and in-store payments through a single integration, Xiaomi can focus on delivering value to its global customers while relying on Adyen for operational efficiency and technical reliability.

🇧🇷 Brazil’s Central Bank argues stablecoins should be regulated as electronic money. The proposal would bring stablecoin issuers under the same supervisory framework as traditional payment institutions, including requirements for capital reserves, consumer protection, and anti-money laundering compliance.

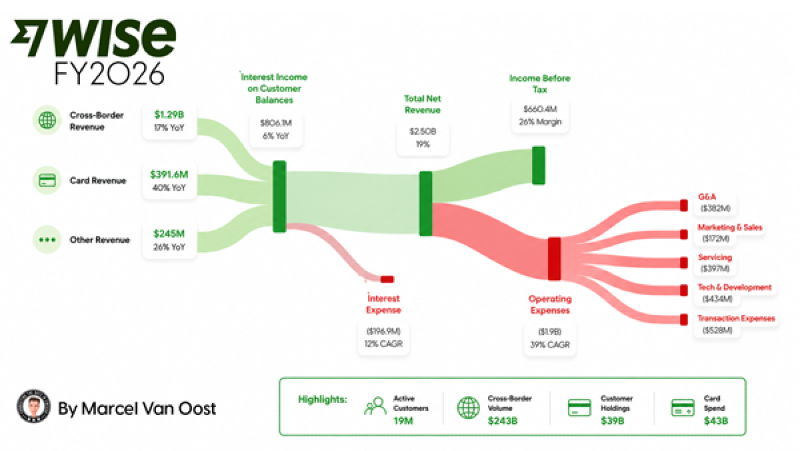

📊 Wise reported FY26 net revenue of $2.5 billion (+19% YoY), $243 billion in cross-border volume (+31%), and 19 million active customers (+21%).

🇸🇬 PingPong Payments secures in-principle approval for a capital markets services licence. This CMS licence will allow PingPong to offer eligible Singapore-based clients over-the-counter FX derivatives products through its subsidiary, Mana Markets. Eligible clients will be able to hedge against foreign exchange volatility.

🇭🇺 Pay10 secures Hungary EMI licence to launch EU operations. The licence enables Pay10 EU to launch regulated electronic money and payment services in Hungary. The company is also preparing a full rollout for both consumers and businesses following the central bank’s decision.

🇮🇳 Visa launches Payment Passkey in India with IDFC FIRST Bank. Visa has said the solution is expected to improve payment success rates while reducing the number of steps required to complete online transactions. Read more

🌍 CaixaBank completes its first transaction initiated by an artificial intelligence agent in collaboration with Visa. The collaboration with Visa through the Agentic Ready programme enables progress towards new customer relationship models, in which artificial intelligence can act on the customer’s behalf using infrastructures that already provide high standards of security and control.

🇬🇧 Pay.UK introduces a flexible liquidity model for Faster Payments Net Sender Caps (NSC), reducing pre-funding requirements for payment service providers. The change lowers barriers to direct participation while maintaining liquidity and risk controls through centralized oversight.

🇪🇺 Revolut to delist USDT for European users as MiCA rules reshape stablecoin access. Revolut has informed affected users via email that it will gradually stop supporting USDT in the coming months. Users can keep purchasing USDT until July 6, after which Revolut will not accept any more purchases of USDT.

🇲🇾 Malaysian FinTech firm AhaPay expands with DirectD. The partnership aims to add BNPL and instalment payments in DirectD’s stores across the country after an initial deployment began in Q2 2026. Continue reading

🇺🇸 MoneyGram appoints Will Karczewski as EVP and General Manager, Global Retail, to accelerate omnichannel growth. In this role, Karczewski will lead the company's global retail and digital partner businesses, helping unlock growth opportunities across its global retail network while advancing the integration of retail and digital customer experiences.

GOLDEN NUGGET

𝐖𝐡𝐲 𝐝𝐨𝐞𝐬 𝐢𝐭 𝐭𝐚𝐤𝐞 5 𝐝𝐚𝐲𝐬 𝐭𝐨 𝐰𝐢𝐫𝐞 $10,000 — 𝐛𝐮𝐭 2 𝐬𝐞𝐜𝐨𝐧𝐝𝐬 𝐭𝐨 𝐬𝐞𝐧𝐝 𝐭𝐡𝐞 𝐬𝐚𝐦𝐞 𝐚𝐦𝐨𝐮𝐧𝐭 𝐢𝐧 𝐔𝐒𝐃𝐂?👇 Created by Arthur Bedel 💳 ♻️

Imagine you send $10,000 across eight different rails at the exact same second.

Which one delivers first?

Most people would guess Visa or PayPal. They feel instant. They look instant.

They are not.

Every "instant" payment you've ever made has hidden a delay you never see — a lag built into the way money has moved for the last 50 years.

Settlement is the part of the journey nobody talks about. Until now.

𝐓𝐡𝐞 𝐟𝐢𝐧𝐚𝐥 𝐥𝐞𝐚𝐝𝐞𝐫𝐛𝐨𝐚𝐫𝐝:

🥇 USDC (Solana) — ~2 seconds — fee $0.001

🥈 SEPA Instant — under 10 seconds — fee €0.20

🥉 Bitcoin — ~10 minutes — fee $3.50

4️⃣ PayPal — instant to 1 day — fee $350

5️⃣ Visa & Mastercard — 1 to 3 days — fee $250

6️⃣ Apple Pay — 1 to 3 days — fee $250

7️⃣ ACH — 1 to 3 days — fee $0.50

8️⃣ Wire / Swift — 1 to 5 days — fee $25–$50+

The same $10,000 settles anywhere from 2 seconds to 5 days — depending entirely on which rail it traveled.

That gap is the central tension shaping #Payments this decade.

For 50 years, card networks won on trust, ubiquity, and dispute rights.

Settlement happened invisibly, on a delay nobody questioned.

That model is now under real pressure.

Stablecoin volume hit $27.6 trillion in 2025 — surpassing Visa and Mastercard combined. FedNow tripled year over year. SEPA Instant became law across the EU.

But speed isn't always the goal.

Cards still offer chargeback protection no stablecoin can replicate. ACH is the cheapest way to move recurring batches. SWIFT remains the only practical option in many cross-border corridors.

Each rail wins a different job.

The real shift isn't replacement. It is intelligent routing.

The CFOs, treasurers, and merchants who win the next decade won't pick one rail. They'll build multi-rail strategies and route every payment to the rail that fits its purpose.

Single-rail thinking is a liability.

Multi-rail intelligence is the new competitive advantage.

Which rail do you think wins the most ground over the next 10 years — stablecoins, instant bank rails, or cards?

Source: Gaspard Lézin

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()