Mastercard Move Expands China Payment Access For Global SMEs

Hey Payments Fanatic!

Mastercard is extending its global money movement infrastructure in China. 🇨🇳

Mastercard Move is now connected to Bank of Shanghai, enabling bi-directional cross-border payments between China and global markets.

That progression is worth watching.

China exports more than $3 trillion each year. Fast and predictable payments are critical for SMEs managing those trade flows. This integration allows global businesses to send funds directly into China’s domestic bank account network.

Mastercard Move already connects to UnionPay cards, Alipay, and WeChat Pay. The platform already operates across 200+ countries and territories, supports 150+ currencies, and reaches nearly 17 billion endpoints worldwide.

Yu Minhua, Deputy President at Bank of Shanghai, added that efficient cross-border capital flows are becoming essential for SMEs and families, especially as Chinese businesses expand into global supply chains.

Pratik Khowala, Global Head of Transfer Solutions at Mastercard, said China sits at the center of how people and money move globally, highlighting the country’s role in cross-border payment flows.

Global payment rails continue to expand. Scroll down 👇 and I will unpack a few more signals shaping the market.

Cheers,

INSIGHTS

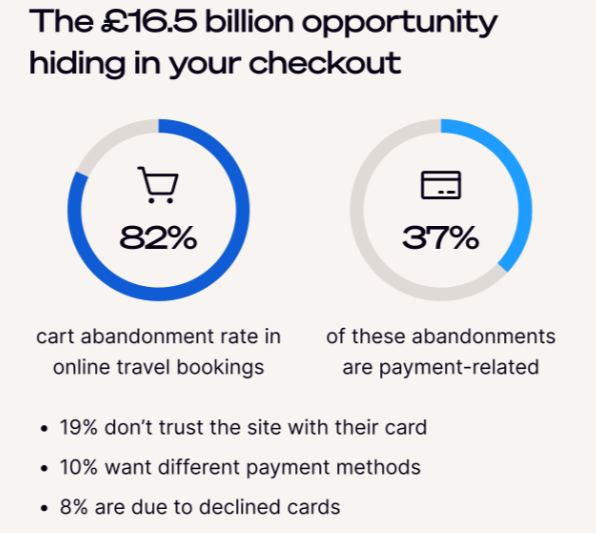

📰 Payments are becoming the battleground for UK travel, by Ecommpay. A new report by Ecommpay analysing the payment strategies of the top 10 UK online travel agencies highlights how checkout has become a key driver of trust, conversion, and revenue. With 81.7% cart abandonment in travel, the study identifies a £16.5 billion opportunity for companies to improve performance. Download the report here

NEWS

🌍 FinTech Airwallex earmarks $1.1 billion for European expansion. The funds will be used to launch in new markets, including Spain and Sweden. The company runs a financial platform that uses AI to help businesses manage multicurrency accounts, process international payments, and run invoicing and expense systems.

🌍 Noah and Hurupay team up to fix global payments for freelancers. The companies have partnered to deliver institutional-grade financial infrastructure to freelancers via smartphones. Through Noah’s API infrastructure, Hurupay provides freelancers with named virtual USD and EUR bank accounts across Indonesia, the Philippines, and beyond.

🇺🇦 Mastercard and the National Bank of Ukraine strengthen cooperation in cybersecurity. The collaboration will focus on sharing threat intelligence, promoting best practices, and improving cyber resilience across Ukraine’s financial ecosystem. Continue reading

🇬🇭 Stanbic Bank, IFC, and Mastercard collaborate to expand access to finance for female-owned SMEs and professionals in Ghana, under IFC’s Banking on Women programme. The companies have committed $600,000 to expand access to capital for female-owned SMEs, strengthen Stanbic Bank’s capacity to serve this segment, and promote gender-responsive banking to support inclusive growth in Ghana.

🇨🇳 Mastercard Move partners with Bank of Shanghai to enable seamless cross-border payments between China and global markets. The collaboration expands connectivity to China’s bank account network, supporting SMEs, remittances, and education payments with faster and more predictable transfers.

🇸🇬 MetaComp has secured $44.45M in Pre-A funding backed by Alibaba and Spark Venture to expand its Web2.5 payments and wealth platform. The funds will support AI development and the rollout of its StableX Network across Asia, the Middle East, Africa, and Latin America.

🇩🇪 Unzer Group acquires AllCash and expands business in eastern Germany. The acquisition adds more than 500 terminals to Unzer’s network, enabling around 2.5 million additional annual transactions and expanding its merchant base in a region where the company plans significant growth.

🇧🇷 Brazil court orders Stone to reinstate laid-off workers, but negotiations pause the decision. A labor court in Brazil ordered Stone to reinstate about 370 employees (around 2% of the company’s 16,700 workforce) dismissed last week, giving the company 10 days to comply.

🇬🇧 Ramp acquires Billhop to expand access for UK and European customers. The acquisition strengthens Ramp’s regional expertise and broadens support for businesses across the region. The company will open its first international offices in London and Stockholm while expanding its European team, with onboarding expected to begin this summer.

🇲🇹 Malta-based Papaya Ltd powers the launch of Blackcat, a new European FinTech app. Blackcat offers a unified financial experience combining euro-based payment services with integrated cryptocurrency functionality. Users receive a personal EUR IBAN, access to SEPA transfers, cards, multiple euro wallets, cashback programmes, and rewards on EUR balances.

🇬🇧 Teybridge Capital Europe plans a €5.2 million UK expansion. As part of its investment in the UK market, Teybridge will create up to 30 new jobs in its London office over the next three years. Additionally, it has committed to deploying €694.9 million (£600 million) during the same period to support British SMEs.

🇺🇸 Plaid and Truist have announced a data-access agreement to expand open banking capabilities for Truist customers. The partnership will introduce FDX-aligned APIs, smoother logins, and shared risk signals, giving users more control over their financial data and connections.

🇸🇻 Tether has named Zachary Lyons as Chief Investment Officer, succeeding Richard Heathcote, who will step back from day-to-day duties and move into a non-executive advisory role. Lyons previously served as deputy CIO and will lead Tether’s investment strategy and capital deployment.

🇸🇪 APPRL co-founder Martin Landén departs Klarna nearly five years after the FinTech acquired his social commerce start-up. Landén led APPRL as CEO until the 2021 deal and later served as Klarna’s head of social shopping, helping build the Klarna Creator Platform. He announced the move on LinkedIn but did not disclose his next career steps.

🇧🇷 Divibank reports a 13-fold increase in revenue after pivoting. According to Divibank, the growth was driven by the expansion of its customer base and demand for payment solutions geared toward digital operations with higher transaction volumes.

🇯🇴 Valu expands to Jordan with $7M, but the payments ecosystem outpaces loan growth. This $ 7 million allocation to Jordan expansion would enable quick penetration into the marketplace, support local partnerships, technological advancement, merchant onboarding, and customer acquisition programs.

🇧🇷 Matera appoints Roberto Otero as Chief Strategy Officer, where he will lead capital markets, investor relations, and M&A. The executive brings more than 15 years of experience, with previous roles at Bank of America, Arco Educação, and Eurofarma.

🇺🇸 MoonPay and Exodus have partnered with the MoonPay X Games League to pay athletes using XO Cash, a USD-backed stablecoin issued by MoonPay. As part of the league’s inaugural Summer Draft, 40 athletes will receive $2,500 signing bonuses in the stablecoin via Exodus wallets, along with NFC-enabled cards for instant spending.

GOLDEN NUGGET

What is interchange, and what factors impact the interchange rate?

Let’s break it down:

Every time a consumer swipes a card to make a purchase, the merchant pays an interchange fee.

Revenue from the fee gets divided among parties that facilitated the transaction: the banks that send and receive the payment, the card network, the payment processor, and—more recently—FinTechs and businesses that embed payments.

When you take the bird-eye view diagram above as an example:

If a user swipes a card issued by a Neobank, $1.70 (interchange fee) goes to the issuing bank and the card network, $0.50 (acquiring fee) goes to the acquiring bank.

Interchange fees are not always the same though.

𝗪𝗵𝗮𝘁 𝗳𝗮𝗰𝘁𝗼𝗿𝘀 𝗶𝗺𝗽𝗮𝗰𝘁 𝗶𝗻𝘁𝗲𝗿𝗰𝗵𝗮𝗻𝗴𝗲 𝗿𝗮𝘁𝗲?

► Credit vs. Debit

Interchange rates on credit cards are significantly higher than those on debit cards.

► Rewards programs

These benefits are financed through higher interchange rates, and have proven to be very popular with consumers.

► Online vs. Offline

Online purchases are less secure than in-person purchases.

► Consumer vs. Commercial

Cards associated with business or corporate accounts carry higher interchange rates than consumer cards.

► Merchant Category Code (MCC)

Every merchant is categorized by the major card networks according to a Merchant Category Code (MCC). This means that there are different interchange rates depending on whether someone uses a card in a supermarket, a retail store, a gas station, or with some other form of merchant.

► The Card Network

Different card networks charge different rates. Visa and Mastercard are known for charging lower rates. Other networks like AMEX are known for charging higher rates.

► Network partner programs

Visa and Mastercard’s partner programs like VPP (Visa Partner Program) and MPP (Mastercard Partner Program) often give specific retailers interchange rates that are much lower than the networks’ published interchange rates.

► Size of the issuing bank (𝗢𝗡𝗟𝗬 in the US 🇺🇸)

Larger banks are subject to a regulation called the Durbin Amendment that caps interchange rates on consumer debit transactions. Smaller banks are exempt.

As a result, these smaller banks can earn more revenue from interchange rates, which benefits FinTechs and embedded finance businesses that partner with them.

Source: Connecting The Dots in FinTech

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()