PayU Reaches a Major Milestone

Hey Payments Fanatic!

PayU India has achieved something many FinTechs spend years chasing: profitability.

The company reported its first full year of positive operating profit, generating $781 million in revenue while turning an EBITDA loss into an $18 million profit. At the same time, it received approval from the Reserve Bank of India to operate as a payment aggregator for online, offline, and cross-border transactions.

The results show that growth isn't the only priority anymore.

Like many mature payments companies, PayU is becoming more focused on improving margins, streamlining its business, and building a more sustainable operating model.

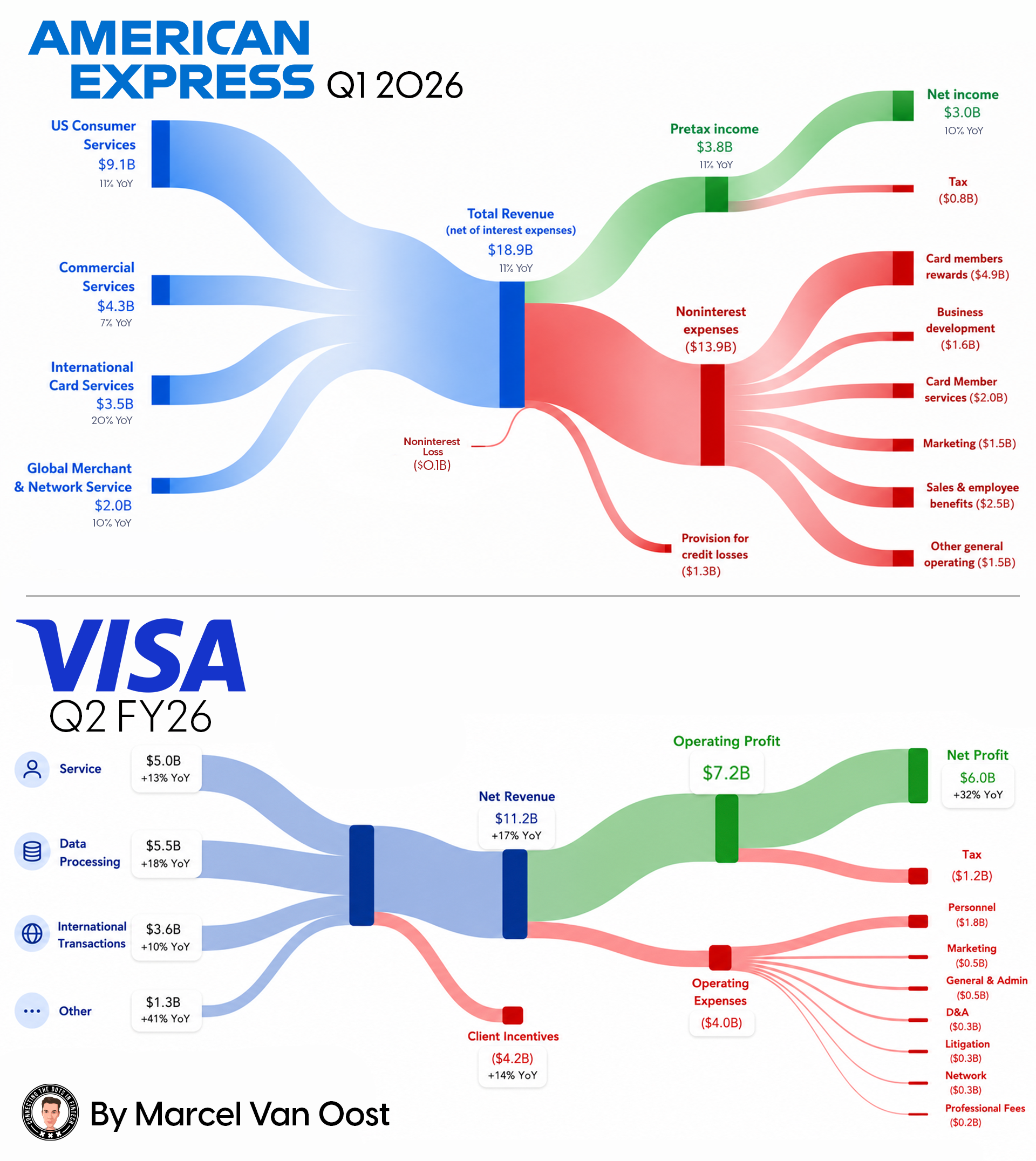

And speaking of payments at scale, keep scrolling for a comparison of American Express and Visa. While both continue benefiting from the global shift toward digital payments, their business models couldn't be more different.

See what else is shaping Payments. 👇 See you tomorrow!

Cheers,

INSIGHTS

📊 American Express 🆚 Visa

Here is a comparison of 𝗞𝗲𝘆 𝗦𝘁𝗮𝘁𝘀:

NEWS

🇧🇩 bKash and Mastercard partner to expand remittance access in Bangladesh. Under the collaboration, bKash will use Mastercard Move to enable remittances sent from abroad to be received directly into bKash mobile wallets. Customers will also be able to access cash through bKash's nationwide network of more than 350,000 agents.

🇵🇭 Maya rolls out prepaid Mastercard and Visa cards made from 100% recycled plastic. The cards will continue to offer the same security, durability, and functionality while helping reduce the company’s reliance on virgin plastic. Cardholders can use the recycled plastic cards for ATM withdrawals and purchases at more than 150 million merchant locations worldwide.

🇮🇳 PayU India reported its first full year of operating profitability in FY2026, posting adjusted EBITDA of $18 million after a $25 million loss the previous year. Backed by Prosus, the FinTech grew revenue 13% to $781 million while improving margins across its payments and credit businesses.

🇦🇪 UAE Central Bank licenses Adyen for expanded operational capabilities. The license allows Adyen to further develop its local capabilities across fraud prevention, emerging payment methods, and unified commerce, while laying the foundation for future technologies such as agentic AI.

🇿🇦 Visa launches B2B payments platform in South Africa with FNB and RMB. The platform is designed to simplify how organisations manage supplier payments, corporate travel, and operational spend. It enables secure virtual card issuance, automates reconciliation, and provides visibility into spending patterns through a centralised interface.

🇺🇸 American Express hires head of stablecoin and blockchain strategy in push for crypto payments. The new role suggests it is exploring stablecoin and blockchain opportunities alongside its core card, lending, and rewards business. Read more

🇻🇳 9Pay becomes a direct payment partner with Visa, driving cross-border payment solutions. By partnering directly with Visa and CyberSource, 9Pay has upgraded its technological capabilities to provide a comprehensive card processing suite capable of offering customized solutions that fulfill complex technical operations specific to various industries.

🇨🇳 Tencent tests TenPayGo mobile app for overseas visitors. The app is part of the company's effort to help foreign travelers navigate the country's highly digital payment system without the usual challenges of setting up local payment methods. Read more.

🇺🇸 BNY expands relationship with Circle and adds to institutional-grade stablecoin enablement services. BNY clients can now hold USDC in their digital asset custody wallets at BNY, and through BNY they can instruct Circle to convert (“mint”) U.S. dollars into USDC and to redeem (“burn”) USDC for U.S. dollars.

🇦🇪 Dubai FinTech AXON raises $1 million for cross-border payments. The company outlined plans to expand infrastructure connecting traditional financial systems with digital assets. Read more

🇩🇰 Januar secures a MiCA licence and raises €1 million. It can now offer fiat payments and stablecoin services under a single regulatory framework across the EEA. Continue reading

GOLDEN NUGGET

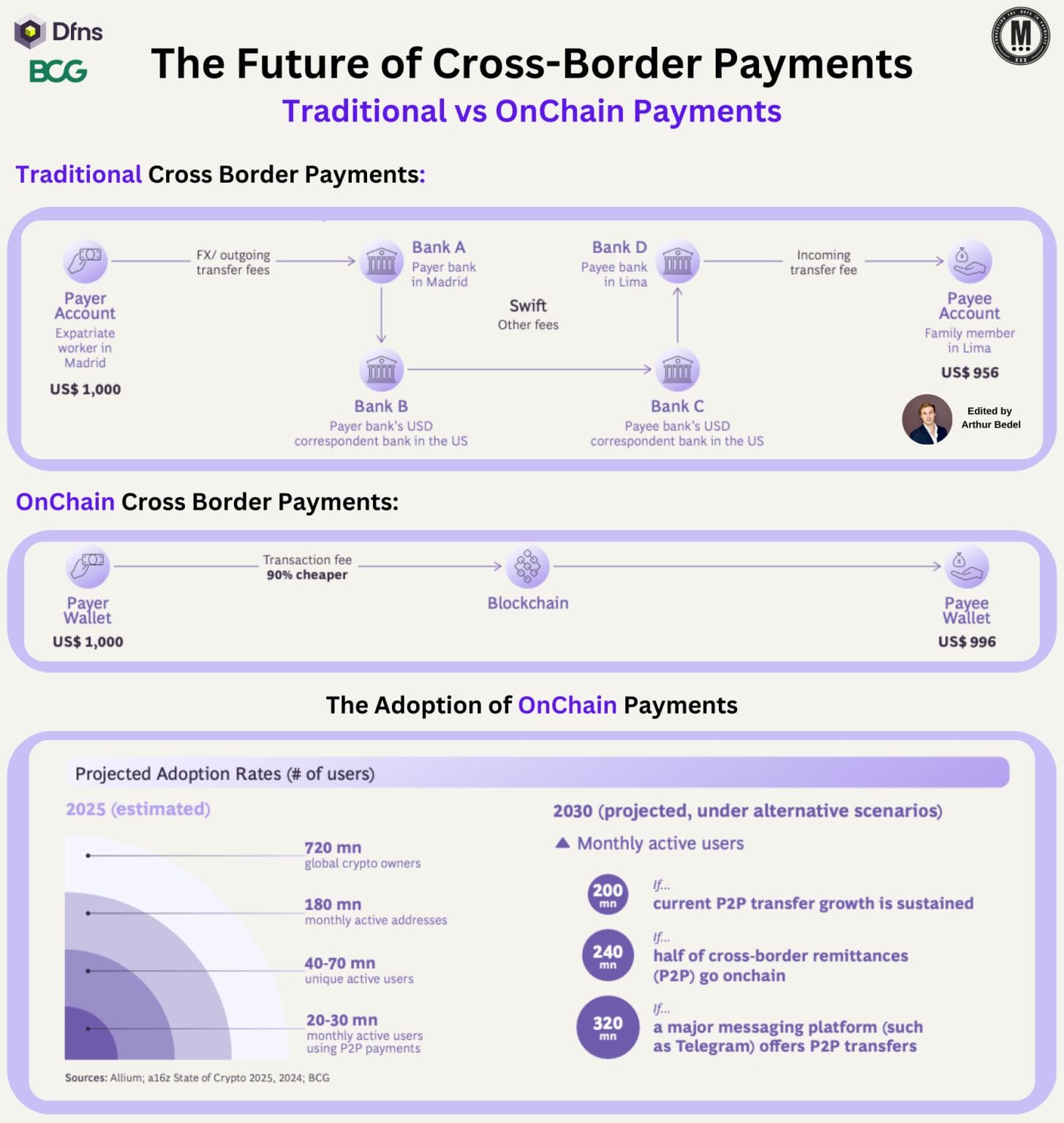

𝐓𝐡𝐞 𝐅𝐮𝐭𝐮𝐫𝐞 𝐨𝐟 𝐂𝐫𝐨𝐬𝐬-𝐁𝐨𝐫𝐝𝐞𝐫 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 — Traditional vs OnChain Payments👇 Created by Arthur Bedel 💳 ♻️

For decades, moving money across borders meant navigating a maze: correspondent banks, cut-off times, FX spreads, SWIFT messages, reconciliation layers... and fees eating away at value.

That model worked for the era of batch banking. It doesn't work for the era of real-time digital commerce.

↳

𝐖𝐡𝐚𝐭 𝐭𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐜𝐫𝐨𝐬𝐬-𝐛𝐨𝐫𝐝𝐞𝐫 𝐚𝐜𝐭𝐮𝐚𝐥𝐥𝐲 𝐥𝐨𝐨𝐤𝐬 𝐥𝐢𝐤𝐞:

A $1,000 transfer can pass through:

• Payer bank

• USD correspondent bank

• Payee correspondent bank

• Payee bank

Each hop = fees + time + opacity.

Result → ~$956 arrives days later.

This isn't a UX problem.

It's an infrastructure problem.

↳

𝐖𝐡𝐚𝐭 𝐎𝐧𝐂𝐡𝐚𝐢𝐧 𝐜𝐡𝐚𝐧𝐠𝐞𝐬:

Instead of messaging layers between banks, value moves directly wallet → wallet on a shared ledger.

• Settlement in seconds

• ~90% lower transaction cost

• Full traceability

• 24/7 availability

• No correspondent chain

Same $1,000 → ~$996 received.

Platforms like Breeze are already turning this into real payment flows, embedding OnChain rails into Merchant-Of-Record (#MOR) and payouts so businesses can settle globally without touching legacy correspondent rails.

That's not incremental improvement.

That's a different operating system.

↳

𝐖𝐡𝐲 𝐜𝐫𝐨𝐬𝐬-𝐛𝐨𝐫𝐝𝐞𝐫 𝐢𝐬 𝐭𝐡𝐞 𝐛𝐞𝐬𝐭 𝐮𝐬𝐞 𝐜𝐚𝐬𝐞 𝐟𝐨𝐫 𝐬𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧 𝐫𝐚𝐢𝐥𝐬 👇

Because the pain is structural:

• Fragmented liquidity

• Multi-day settlement

• FX friction

• Limited operating hours

• Heavy reconciliation

OnChain collapses those layers into one atomic transaction. The payment becomes data + value moving together.

↳

𝐁𝐮𝐭 𝐭𝐡𝐢𝐬 𝐨𝐧𝐥𝐲 𝐰𝐨𝐫𝐤𝐬 𝐰𝐢𝐭𝐡 𝐭𝐡𝐞 𝐫𝐢𝐠𝐡𝐭 𝐰𝐚𝐥𝐥𝐞𝐭 𝐢𝐧𝐟𝐫𝐚

Institutions don't need "more crypto tools." They need bank-grade operating rails for digital assets:

• Policy-driven transaction governance

• MPC/HSM key management

• Compliance & identity controls

• Workflow approvals

• Secure bridging between TradFi & OnChain

That's where Dfns fits — providing the wallet infrastructure layer that lets hashtag

#Banks, #PSPs, and #FinTechs run OnChain payments.

Not DeFi vs TradFi.

→ 𝐓𝐫𝐚𝐝𝐅𝐢 𝐨𝐧 𝐧𝐞𝐰 𝐫𝐚𝐢𝐥𝐬.

↳

𝐖𝐡𝐚𝐭 𝐭𝐡𝐞 𝐧𝐞𝐱𝐭 𝟓 𝐲𝐞𝐚𝐫𝐬 𝐥𝐨𝐨𝐤 𝐥𝐢𝐤𝐞

• Wallet-to-wallet remittances embedded in banking apps

• Treasury moving liquidity OnChain between entities

• PSPs settling payouts in minutes instead of days

• FX happening at protocol level

• Stablecoin rails powering B2B flows

We won't call this "blockchain payments."

We'll just call it... payments.

↳

The future of cross-border isn't another messaging standard. It's a new infrastructure.

🚨 What cross-border flow would you move OnChain first — remittances, payouts, or treasury?

Source: Dfns & Boston Consulting Group (BCG)

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()