PhotonPay and Mastercard Complete First Agentic Payment

Hey Payments Fanatic!

In a live operational demonstration, PhotonPay announced a milestone in an agentic transaction together with Mastercard.

You might be wondering how it worked. Turns out a PhotonPay tokenized card was securely provisioned for use by an AI agent, which autonomously initiated and completed a real-world payment transaction on behalf of a user.

PhotonPay provides the foundation, leveraging real-time settlement capabilities and native API orchestration, while Mastercard Agent Pay provides authentication and security mechanisms for transactions initiated by AI agents.

What excites me most is how quickly this is all becoming real.

Agentic payments are moving from the whiteboard concept to live infrastructure at a pace that should have every payment professional paying close attention.

Keep scrolling for the rest of today's Payments’ stories. 👇 See you on Monday!

Cheers,

INSIGHTS

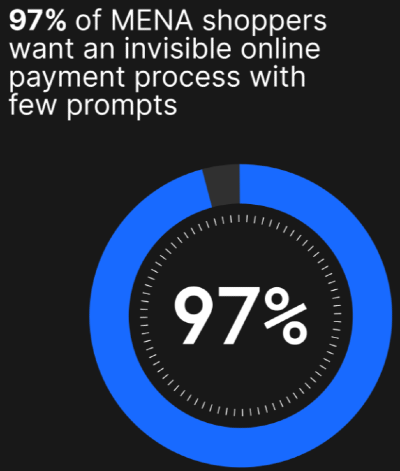

📰 MENA Digital Commerce 2026 by Checkout.com. The New Era of AI in Payments. The report highlights growing demand for seamless, secure, and personalized payment experiences as e-commerce adoption accelerates across the Middle East and North Africa. Download the report here

NEWS

🇭🇰 PhotonPay completes its first live agentic payment together with Mastercard. The project highlights the growing development of “agentic payments,” combining AI decision-making with programmable financial infrastructure, real-time settlement, and secure authentication to support automated and compliant digital commerce.

🇩🇴 Mastercard brings together ecosystem leaders in the Dominican Republic to accelerate the next stage of digital payments. Mastercard Day event highlighted the country’s strong adoption of contactless payments, alongside the opportunity to expand digital payment acceptance among small businesses, while emphasizing collaboration, innovation, and public policy.

🇦🇺 Australian FinTech pioneer Zip Co forced to rebrand its local products and services. Zip has stated that the company is prepared for this outcome and will use this opportunity to evolve its Australian brand to ensure it best reflects its role as a digital-first financial services provider.

🇺🇸 Global Payments unveils AI-first genius handheld built for the future of commerce. The innovative handheld will feature groundbreaking new AI-powered voice ordering technology, which will allow servers to have real conversations with customers while the POS quietly builds the ticket in the background, even in high-noise environments.

🇵🇱 Poland’s BLIK joins pan-European cashless payment push. The partnership aims to connect local mobile payment providers, enabling seamless transactions between different payment systems, currencies, and countries while strengthening interoperability in the European digital payments market.

🇸🇦 Tamara’s profits surge 378% to SAR 123 million in Q1. The growth was driven by higher transaction volumes, expanding merchant and user adoption, and continued demand for buy now, pay later services across sectors such as e-commerce, retail, travel, and digital services.

🇺🇸 Klarna reported strong first-quarter 2026 results, with revenue rising 44% year over year to $1 billion, gross merchandise volume reaching $33.7 billion, and adjusted operating profit increasing to $68 million from $3 million a year earlier. The company also expanded to more than one million merchants and 119 million active consumers.

🇺🇸 Fiserv and Bridgeport partners agree to form a joint Venture to accelerate growth across ATM and cash services businesses. Bridgeport Partners is expected to assume operational control of the businesses and oversee day-to-day management. A formal governance structure will be established, with both parties aligned on long-term value creation, client outcomes, and sustainable growth.

🇺🇸 Circle pitches stablecoin settlement as an alternative to batch banking systems. Circle is expanding its focus on institutional payments infrastructure, arguing that stablecoin-based settlement systems can replace traditional batch-processing models used in global finance.

🇬🇧 Deel and Arsenal announce multi-year sleeve partnership. Deel's logo will appear on the left sleeve of Arsenal's home, away, and third kit shirts from the start of the 2026/27 season. Read more

🇦🇺 NAB acquires FinTech Banked, making payments easier for more businesses. The acquisition strengthens NAB’s innovative payments capability and aligns with its strategy to help more businesses receive payments faster and at a lower cost. Keep reading

🇳🇱 Adyen's collaboration with SAP supports the launch of SAP Unified Payment: a native payment solution for SAP Commerce Cloud. This native, fully embedded solution is designed to remove the structural complexity of global commerce by connecting digital storefronts directly to the financial backbone of the enterprise.

🇺🇸 Shift4 partners with Lydian to support USDT Payment Acceptance. The Lydian partnership adds Tether, a top stablecoin, to the list of crypto payment options supported on the platform, with no new workflows or crypto expertise needed from merchants.

🇨🇴 Oobit launches in Colombia as Latin America’s $44B crypto market surges. Backed by Tether, Oobit says users across the region are increasingly using crypto, particularly USDT, for everyday purchases such as groceries, restaurants, fuel, and retail services, reflecting growing real-world adoption of digital assets in Latin America.

🇺🇸 Payway and Chargebee partner to streamline subscription payments and reduce revenue loss. The integration allows subscription-based businesses using Chargebee to process payments directly through Payway’s gateway without custom development, simplifying recurring billing operations while helping to reduce failed payments, involuntary churn, and manual reconciliation work.

GOLDEN NUGGET

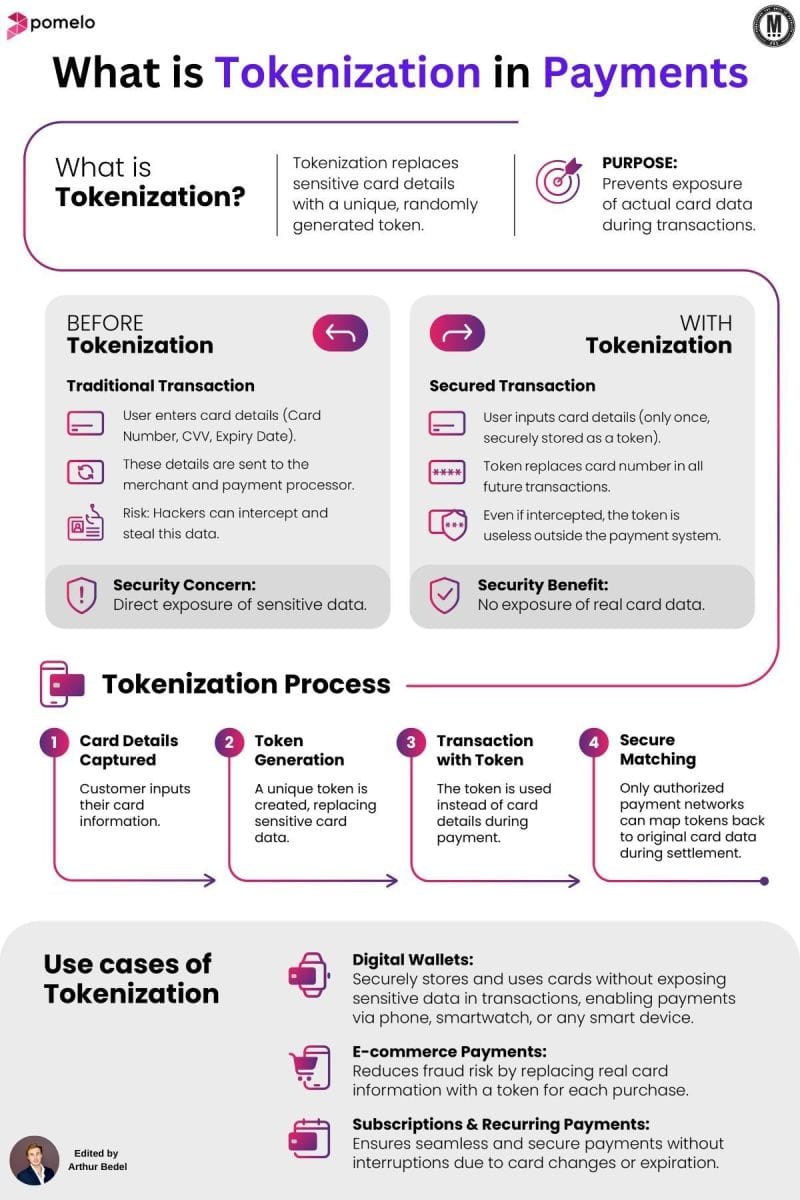

Understanding 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 and 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐒𝐞𝐜𝐮𝐫𝐢𝐭𝐲 by Pomelo👇

𝐃𝐞𝐟𝐢𝐧𝐢𝐭𝐢𝐨𝐧 𝐨𝐟 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐢𝐧 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬:

► Tokenization replaces sensitive card details with a unique, randomly generated token, ensuring that actual card data is never exposed during transactions.

𝐏𝐮𝐫𝐩𝐨𝐬𝐞 𝐨𝐟 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧

► The main goal of Tokenization is to prevent the exposure of sensitive card details, reducing the risk of fraud and unauthorized transactions.

𝐁𝐞𝐟𝐨𝐫𝐞 𝐚𝐧𝐝 𝐖𝐢𝐭𝐡 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧

𝐁𝐞𝐟𝐨𝐫𝐞 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 (𝐓𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧𝐬)

► Users enter card details (Card Number, CVV, Expiry Date).

► These details are sent to the merchant and payment processor.

► Security Concern: Hackers can intercept and steal this data.

𝐖𝐢𝐭𝐡 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 (𝐒𝐞𝐜𝐮𝐫𝐞𝐝 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧𝐬)

► Users enter card details only once, which are securely stored as a token.

► The token replaces the card number in all future transactions.

► Even if intercepted, tokens are useless outside the payment system.

► Security Benefit — No exposure of real card data.

𝐓𝐡𝐞 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐏𝐫𝐨𝐜𝐞𝐬𝐬

1️⃣ 𝐂𝐚𝐫𝐝 𝐃𝐞𝐭𝐚𝐢𝐥𝐬 𝐂𝐚𝐩𝐭𝐮𝐫𝐞𝐝

► The customer inputs their card information at checkout.

2️⃣ 𝐓𝐨𝐤𝐞𝐧 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐢𝐨𝐧

► A unique token is created, replacing sensitive card data. There are several type of tokens — Merchant, PSP, Network Tokens etc...

3️⃣ 𝐓𝐫𝐚𝐧𝐬𝐚𝐜𝐭𝐢𝐨𝐧 𝐰𝐢𝐭𝐡 𝐓𝐨𝐤𝐞𝐧

► The token is used instead of card details during payment.

4️⃣ 𝐒𝐞𝐜𝐮𝐫𝐞 𝐌𝐚𝐭𝐜𝐡𝐢𝐧𝐠

► Only authorized payment networks can map tokens back to the original card during settlement.

𝐔𝐬𝐞 𝐂𝐚𝐬𝐞𝐬 𝐨𝐟 𝐓𝐨𝐤𝐞𝐧𝐢𝐳𝐚𝐭𝐢𝐨𝐧

► 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐖𝐚𝐥𝐥𝐞𝐭𝐬 – Securely store and use cards without exposing sensitive data when making payments via phone, smartwatch, or any smart device.

► 𝐄-𝐜𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 – Reduces fraud risk by replacing real card details with a token for each transaction.

► 𝐒𝐮𝐛𝐬𝐜𝐫𝐢𝐩𝐭𝐢𝐨𝐧𝐬 & 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 – Ensures seamless and secure payments, preventing service interruptions due to card expiration or changes.

Source: Arthur Bedel 💳 ♻️ & Pomelo

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()