UPI Heads to Japan… and India’s Payment Rails Go Global Again

Hey Payments Fanatic!

India’s UPI is preparing to debut in Japan, marking another step in the global rollout of the country’s flagship payment network.

A partnership between NTT Data and the National Payments Corporation of India will kick off a trial in fiscal 2026.

The first use case is clear and practical. Indian tourists in Japan will be able to pay using UPI, with transactions debited directly from their bank accounts back home. No new wallets. No cards. No friction.

What’s more interesting is what comes next. NTT Data and NPCI are also exploring deeper links between Japanese and Indian payment networks, pushing cross-border account-to-account payments closer to reality.

UPI keeps doing what it does best. Start local. Prove scale. Then quietly export the rails.

Scroll down to see what else is moving in Payments today 👇 Back tomorrow with more stories.

Cheers,

INSIGHTS

Payment Gateway 🆚 Payment Orchestration

NEWS

🌍 Finby signs up for Wero. Developed by the EPI, Wero aims to create a common digital payment solution across Europe, reducing fragmentation and strengthening European payment sovereignty. By working with EPI, Finby reinforces its role as a payments partner focused on scalable, local-first, and future-oriented technologies.

🇦🇪 Checkout.com expands its enterprise footprint with a deal with Majid Al Futtaim. According to Checkout.com, the implementation has delivered a 3% uplift in payment acceptance rates across the group, centralized fraud visibility with real-time detection, reduced cross-border costs through localized acquiring, and consolidation of payments into a single platform.

🇯🇵 UPI to debut in Japan. Japanese IT services firm NTT Data is partnering with the National Payments Corporation of India (NPCI) to enable UPI acceptance in Japan on a trial basis in fiscal 2026. In the initial phase, the service will be available to Indian tourists visiting the country.

🇺🇸 Apple's Siri Payments begin after claims the assistant recorded personal moments. Apple's long-awaited payouts are now being distributed to individuals who filed claims, offering compensation for alleged privacy intrusions stemming from unintended Siri activations during personal conversations.

🌍 Jelou raises $10M to build transactional AI for WhatsApp. At the centre of Jelou’s strategy is Brain, a platform designed to help businesses build operational agents that carry out real tasks rather than just provide scripted responses. With the new funding, Jelou will expand Brain across the Americas and deepen its capabilities around secure transaction execution inside messaging interfaces.

🇳🇬 Nigerian FinTech OneDosh secures $3m to expand stablecoin payments. Operating in both the U.S. and Nigeria, the platform enables rapid transfers, stablecoin storage, and payments via Apple Pay and Google Pay-compatible cards. The capital will fuel expansion into new payment corridors and the growth of its engineering teams.

🇺🇸 Fiserv and Affirm join forces to bring pay-over-time capabilities to debit card programs for financial institutions. This collaboration empowers thousands of Fiserv U.S. bank and credit union clients to meet growing consumer demand for flexible payment options without needing to build new lending products.

🇮🇹 Nexi Group joins Agentic Commerce Alliance to shape the future of AI-driven commerce. As a member, Nexi will bring European scale, local payment knowledge, and real-world experience in securing the transactional layer for AI agents to help develop open standards that enable trustworthy, interoperable agentic systems.

🇮🇹 Nexi appoints Piergiorgio Pedron as New Group CFO, effective April 1, 2026. At the same time, Nexi revealed that Bernardo Mingrone will take on the role of CEO of Nexi Payments and Chief Regional Officer for Italy. Read more

🇺🇸 PayPal faces backlash as three affiliate networks suspend partnerships, Rakuten Advertising, impact.com, and Awin, following allegations of fraud and non-compliance. The move cuts Honey off from thousands of retail partners and follows claims that the tool interfered with attribution and misled users on discounts.

🇦🇪 UAE's Wio Bank inks partnership with Global FinTech Pine Labs to modernise merchant acquiring infrastructure. The collaboration is going to build a modern acquiring infrastructure for Wio Bank with no legacy tech dependency, enabling faster merchant onboarding, real-time settlement capabilities, and seamless multi-mode payment acceptance at scale.

🇬🇧 Campaigner launches £1.5bn legal action in UK against Apple, claiming the US tech company blocked competition and charged hidden fees that ultimately harmed 50 million UK consumers. The lawsuit targets Apple Pay, which they say has been the only contactless payment service available to iPhone users in Britain over the past decade.

🇸🇦 Ripple signs MOU with Jeel, Riyadh Bank’s innovation arm for blockchain solutions. Ripple and Jeel plan to develop several financial technology applications under the agreement, including cross-border payments and digital asset custody. Keep reading

🇦🇺 Australian digital bank in1bank to cease operations. The bank says customers have until 4th February 2026 to transfer remaining balances to alternate bank accounts, adding on its website: "Please note that the in1bank app will no longer be in service, effective at 5 pm AEDT on 5th February 2026."

GOLDEN NUGGET

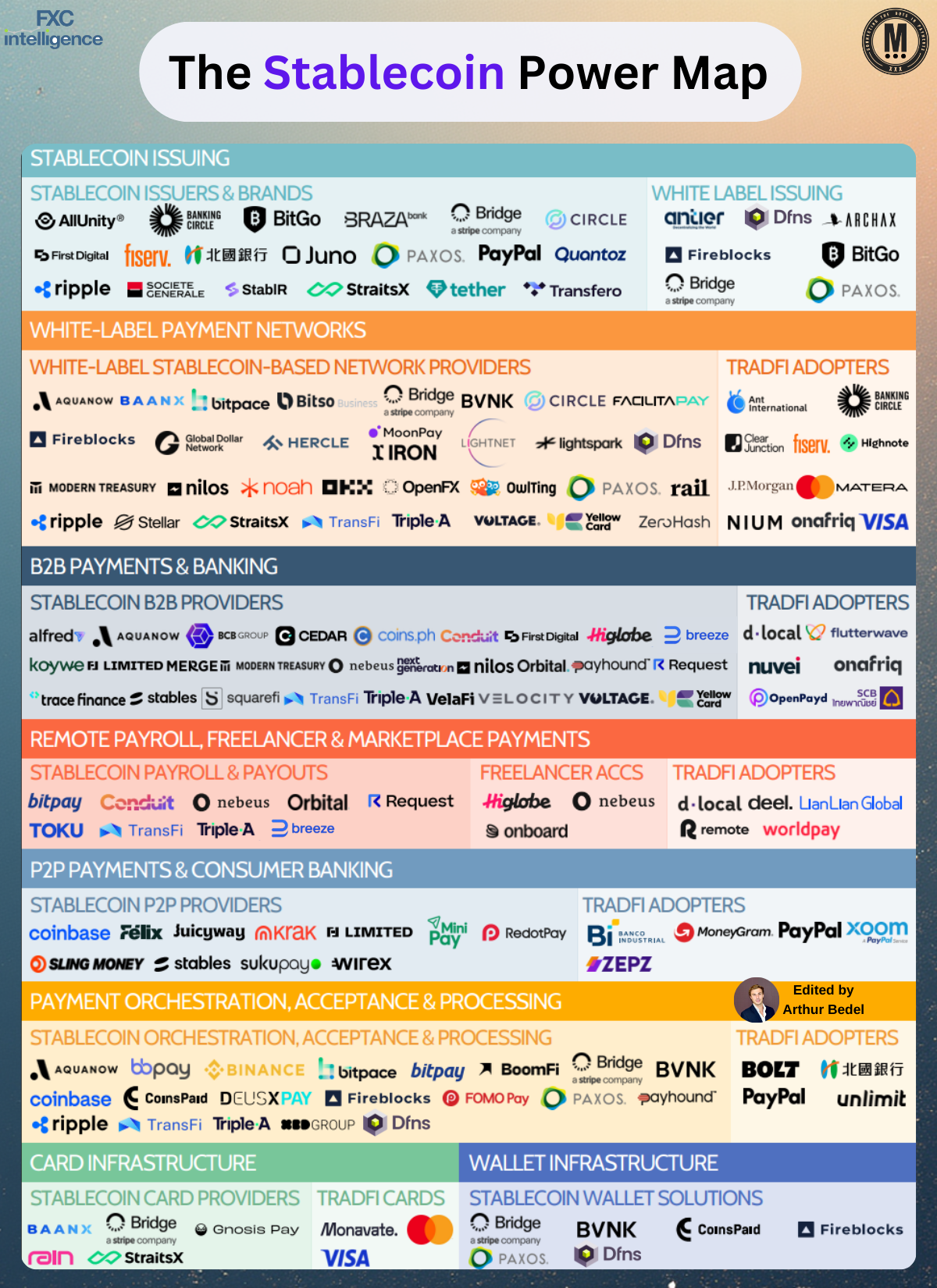

𝐓𝐡𝐞 𝐒𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧 𝐏𝐨𝐰𝐞𝐫 𝐌𝐚𝐩 — understanding today’s ecosystem 👇 Created by Arthur Bedel 💳 ♻️

Stablecoins now move trillions annually. FXC Intelligence’s Stablecoin Power Map clarifies how value flows across issuers, liquidity networks, orchestration layers, payouts, wallets and enterprise platforms — showing how stablecoins are a programmable settlement layer in global commerce.

Here is a clear view of the core layers defining the stablecoin economy.

𝐓𝐡𝐞 𝐒𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧 𝐋𝐚𝐲𝐞𝐫𝐬 — explained

1️⃣ 𝐈𝐬𝐬𝐮𝐞𝐫𝐬 & 𝐖𝐡𝐢𝐭𝐞-𝐋𝐚𝐛𝐞𝐥 𝐈𝐬𝐬𝐮𝐢𝐧𝐠

→ Role: Create stablecoins and operate issuance, mint/burn, reserve, and treasury frameworks.

→ Providers: Circle, Tether.io, Paxos, PayPal, Ripple, Dfns.

↳ Paxos continues to scale regulated white-label issuance frameworks, supported by wallet infrastructure providers like Dfns.

2️⃣ 𝐍𝐞𝐭𝐰𝐨𝐫𝐤 & 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲 𝐏𝐫𝐨𝐯𝐢𝐝𝐞𝐫𝐬

→ Role: Deliver liquidity, FX, routing, compliance, and programmable settlement rails across global corridors.

→ Providers: BVNK, Bitso, Lightspark

↳ Lightspark and Noah are building next-generation settlement networks.

3️⃣ 𝐁2𝐁 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 & 𝐄𝐧𝐭𝐞𝐫𝐩𝐫𝐢𝐬𝐞 𝐁𝐚𝐧𝐤𝐢𝐧𝐠

→ Role: Power global merchants, marketplaces, exporters, airlines and platforms with faster settlement and less FX friction.

→ Providers: Conduit, Orbital, Triple-A, Breeze

↳ Breeze is driving new MoR settlement models that embed blockchain logic into global merchant operations.

4️⃣ 𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐏𝐚𝐲𝐨𝐮𝐭𝐬 & 𝐌𝐚𝐫𝐤𝐞𝐭𝐩𝐥𝐚𝐜𝐞𝐬

→ Role: Support creator payouts, freelancers, gig-economy disbursements, and marketplace settlements.

→ Providers: Bitwage, Request Finance, TransFi

↳ BitPay enables global platforms to incorporate stablecoin payouts.

5️⃣ 𝐏2𝐏 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 & 𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐁𝐚𝐧𝐤𝐢𝐧𝐠

→ Role: Enable remittances, consumer wallets, debit cards, and stablecoin accounts.

→ Providers: Coinbase, Kraken, Stables.

↳ Coinbase is integrating stablecoin transfers and spend into mainstream consumer financial experiences.

6️⃣ 𝐎𝐫𝐜𝐡𝐞𝐬𝐭𝐫𝐚𝐭𝐢𝐨𝐧, 𝐏𝐫𝐨𝐜𝐞𝐬𝐬𝐢𝐧𝐠 & 𝐀𝐜𝐜𝐞𝐩𝐭𝐚𝐧𝐜𝐞

→ Role: Manage routing, FX, treasury automation, and multi-rail acceptance across fiat and stablecoin flows.

→ Providers: Aquanow, BitPay, Fireblocks, Bridge.

↳ Bridge is building orchestration frameworks that unify fiat and stablecoin.

7️⃣ 𝐂𝐚𝐫𝐝 & 𝐖𝐚𝐥𝐥𝐞𝐭 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞

→ Role: Provide embedded wallets, card programs, tokenized balances, and programmable enterprise accounts.

→ Providers: Gnosis Pay, BVNK, Ripple, Dfns.

↳ Dfns delivers programmatic wallet infrastructure enabling enterprises to embed stablecoin functionality securely at scale.

Stablecoins aren’t replacing traditional finance — they’re extending it, forming a more programmable and globally accessible liquidity layer.

Source: FXC Intelligence

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()