Beyond Poland: BLIK Hits New Highs in Q1

Hey Payments Fanatic!

Polish payments giant BLIK shows no signs of slowing down.

Fresh data for Q1 2026 reveals that users completed 756 million transactions, a 14% jump year-over-year. This momentum is further underscored by a total transaction volume of PLN 117.3 billion (€27.6 billion).

E-commerce remains the engine of this growth, with the online channel accounting for 50.1% of all BLIK operations. However, the narrative is shifting from domestic dominance to international ambition.

Dariusz Mazurkiewicz, CEO of Polish Payment Standard (BLIK’s operator), noted that they are “consistently expanding the system’s availability beyond Poland.”

“The first successful transactions in Slovak e-commerce strengthen our strategy of building an interoperable solution in Europe. This opens the way for users to make convenient payments on foreign platforms across the eurozone,” said Mazurkiewicz.

As I covered last month, BLIK is officially entering the Eurozone, starting with its rollout in Slovakia.

Keep scrolling to see what else is shaking up the payments world. 👇 Catch you in tomorrow's edition!

Cheers,

INSIGHTS

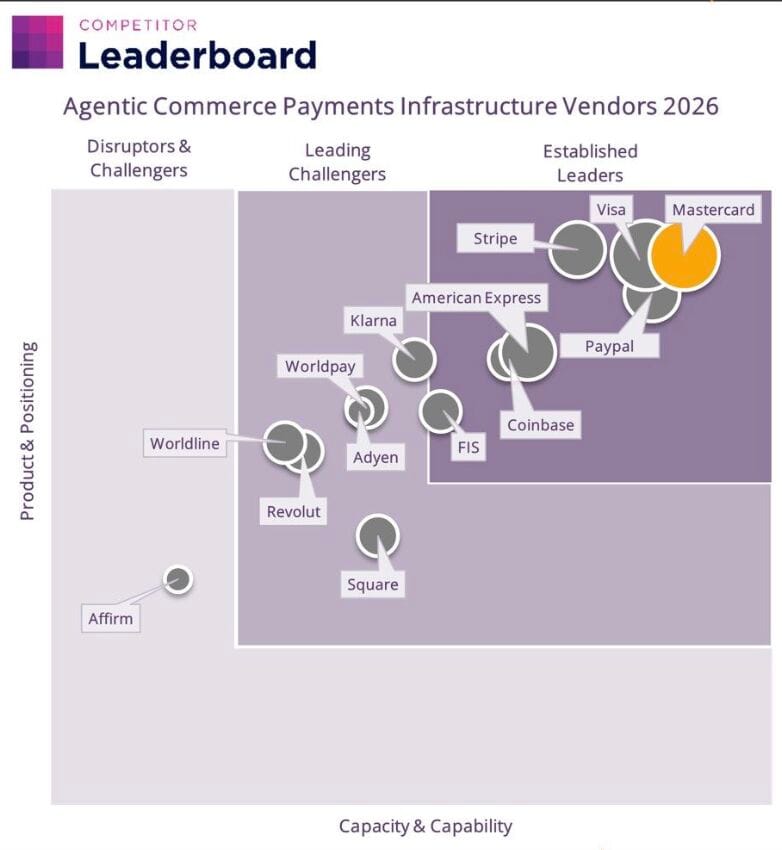

📊 Agentic commerce is expected to reach $𝟭.𝟱 𝗧𝗥𝗜𝗟𝗟𝗜𝗢𝗡 by 2030 🤯

NEWS

🇳🇬 BMONI and Mastercard collaborate to unlock instant card access for consumers in Nigeria. The collaboration aims to introduce a new generation of virtual and physical payment cards designed to enable seamless local and global transactions for consumers in the country.

🇵🇹 Mastercard completes first ‘real-world AI agent transaction’ in Portugal using credentials from a Portuguese payment card, marking a milestone for agentic commerce. The demonstration took place during the launch of Mastercard’s Innovation Centre of Excellence in Lisbon, highlighting the company’s growing focus on AI, cybersecurity, fraud prevention, and next-generation payment infrastructure.

🌎 Mastercard appoints Florencia Solazzi as the new Cluster Leader for Argentina and Uruguay. In this role, Florencia will be responsible for defining and executing Mastercard's strategy, leading business operations, customer, regulatory, and strategic partner relationships, and consolidating a growth model based on innovation, scale, and operational excellence.

🇵🇱 BLIK processed 756 million transactions worth nearly PLN 120 billion in Q1 2026, maintaining double-digit growth driven largely by e-commerce activity. Online payments accounted for half of all transactions, with newer services like recurring payments and Buy Now, Pay Later contributing to increased adoption among its 21.1 million active users.

🇬🇧 PayDo partners with BVNK to add stablecoin pay-ins, payouts, and checkout capabilities, without requiring them to directly handle crypto. By adding stablecoins to its payment stack, PayDo is offering its business customers greater flexibility, speed, and choice when it comes to moving money.

🇭🇰 RedotPay boards Tempo to deliver agentic payments using stablecoins. By integrating Tempo’s Machine Payments Protocol (MPP), RedotPay is spearheading agentic payments to deliver a convenient, fully automated stablecoin payment solution for consumers and merchants.

🇨🇦 Visa Canada and Wealthsimple pilot stablecoin settlement. Through this pilot, Wealthsimple can now satisfy certain settlement obligations with Visa Canada in USD Coin (USDC), bringing stablecoin settlement to the Canadian market.

🇺🇸 PayPal hires Antonio Lucio as new CMO amid restructuring. The company is reorganizing into three core business units, including Venmo and crypto services, as it looks to accelerate growth, streamline operations, and strengthen its long-term innovation strategy.

🇳🇱 Currensea expands into Europe after securing Dutch regulatory approval. The approval enables Currensea to roll out its co-branded debit card platform throughout the European Economic Area in partnership with airlines, hotel groups, and other major brands.

🇨🇳 Geidea and UnionPay roll out dual-card routing upgrade in MEA. The integration aims to reduce friction for Chinese tourists and expatriates by enabling them to use their cards with a level of familiarity similar to that in their home market.

🇬🇧 Thredd and Currensea expand strategic partnership to power next phase of growth. Thredd provides the issuer processing and core programme infrastructure underpinning Currensea’s debit card offering, supporting both physical and virtual cards, tokenisation, digital wallet provisioning, and secure transaction processing.

🌏 Yuno partners with Tabby to enable Buy Now, Pay Later for merchants across the MENA Region. The integration helps merchants tap into one of the region’s most widely used payment methods, supporting higher conversion rates and broader access to underbanked consumers in the GCC.

🇺🇸 StoneX not to make an offer for CAB Payments. The decision ends, for now, a high-profile takeover battle over the London-listed payments firm, though StoneX left open the possibility of revisiting a bid under certain future conditions. Read more

🌎 Bitget enables scan to pay for instant payments via USDT. The feature is now live across selected markets in Southeast Asia and Latin America at launch. By integrating with existing local payment networks, Scan to Pay allows users to complete transactions without changing merchant systems or relying on bank intermediaries.

GOLDEN NUGGET

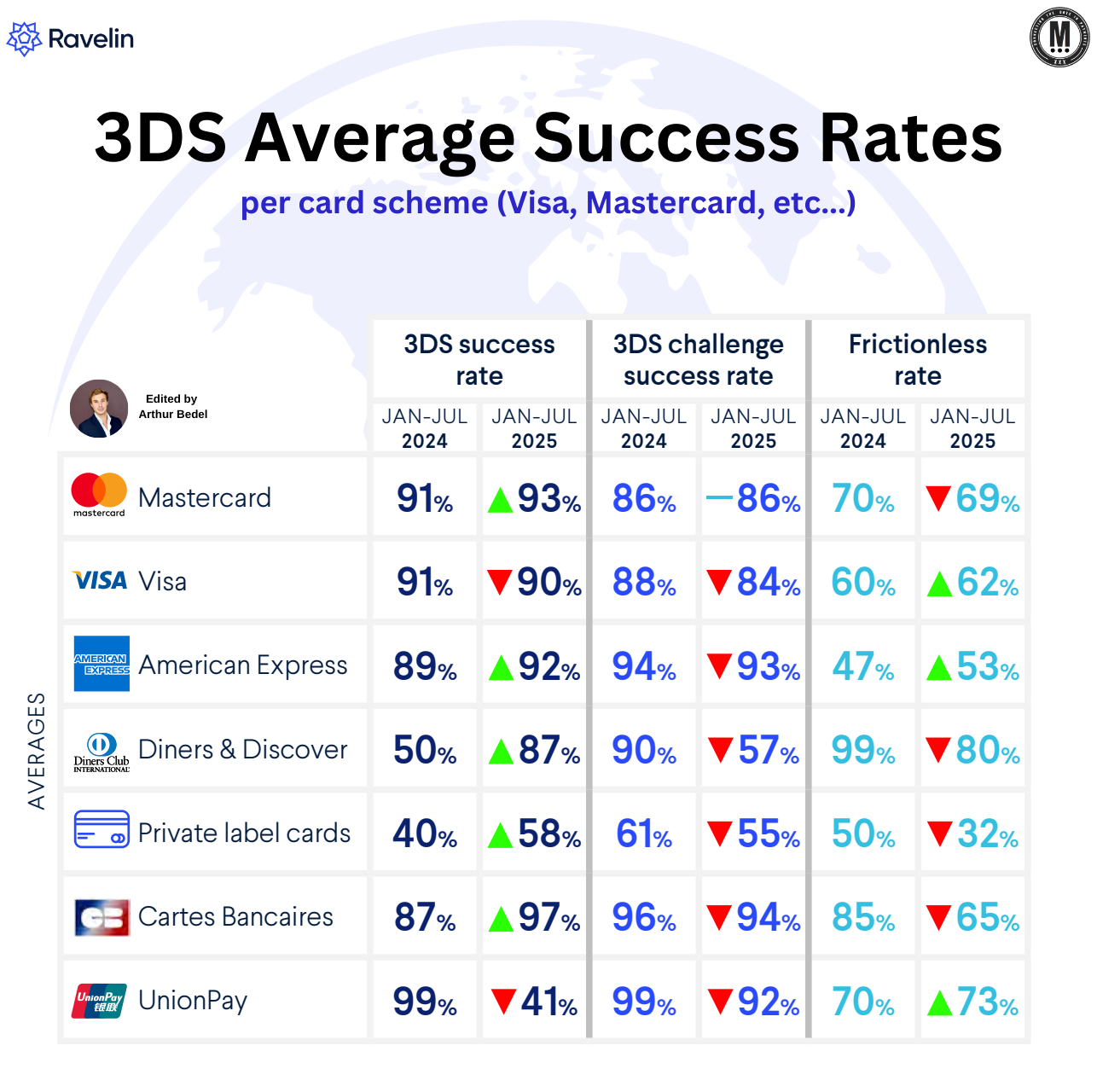

3𝐃𝐒 𝐀𝐯𝐞𝐫𝐚𝐠𝐞 𝐒𝐮𝐜𝐜𝐞𝐬𝐬 𝐑𝐚𝐭𝐞𝐬 𝐩𝐞𝐫 𝐂𝐚𝐫𝐝 𝐒𝐜𝐡𝐞𝐦𝐞 - the real story, frictionless is declining - by Ravelin Technology 👇Created by Arthur Bedel 💳 ♻️

On the surface, authentication performance looks stable — even improving.

→ Global 3DS success rate: 79% → 82%

→ 3DS challenge success rate: 74% → 76%

→ Frictionless rate: 64% → 58%

Frictionless declined in 76% of countries. That’s not noise. That’s structural.

↳

𝐓𝐡𝐞 𝐌𝐢𝐬𝐥𝐞𝐚𝐝𝐢𝐧𝐠 𝐌𝐞𝐭𝐫𝐢𝐜

𝐀 𝐫𝐢𝐬𝐢𝐧𝐠 3𝐃𝐒 𝐬𝐮𝐜𝐜𝐞𝐬𝐬 𝐫𝐚𝐭𝐞 𝐝𝐨𝐞𝐬 𝐧𝐨𝐭 𝐧𝐞𝐜𝐞𝐬𝐬𝐚𝐫𝐢𝐥𝐲 𝐬𝐢𝐠𝐧𝐚𝐥 𝐛𝐞𝐭𝐭𝐞𝐫 𝐩𝐞𝐫𝐟𝐨𝐫𝐦𝐚𝐧𝐜𝐞. If more transactions are challenged — and customers successfully complete those challenges — “success” increases.

But conversion does not.

Frictionless is the real proxy for authentication quality.

And it is under pressure globally.

↳

𝐖𝐡𝐚𝐭’𝐬 𝐃𝐫𝐢𝐯𝐢𝐧𝐠 𝐓𝐡𝐢𝐬?

→ Issuers tightening fraud thresholds

→ Exemptions approved less frequently

→ Scheme monitoring intensifying

→ Expanding regulatory scrutiny

Merchants are requesting more exemptions. Issuers are granting fewer. The tension shows up directly in the frictionless data.

↳

𝐓𝐡𝐞 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐈𝐦𝐩𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧 - 3DS is no longer a compliance layer.

It is a dynamic optimization challenge — issuer by issuer, transaction by transaction.

The advantage is no longer connectivity. It is authentication intelligence:

→ Richer authorization data

→ Adaptive exemption logic

→ Network token optimization

→ Continuous issuer feedback learning

𝐓𝐡𝐞 𝐪𝐮𝐞𝐬𝐭𝐢𝐨𝐧 𝐢𝐬 𝐧𝐨 𝐥𝐨𝐧𝐠𝐞𝐫:

“Are you using 3DS?”

𝐈𝐭’𝐬:

“Are you optimizing it?”

As Nike said: Just do it. 🚀

Payments, they never stops...

Source: Ravelin Technology - Global Payments Report 2026

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()