Brazil's Central Bank Tightens Control Over Digital Payments

Hey Payments Fanatic!

Brazil's regulator is sending a clear message this week: the country wants tighter oversight of its rapidly evolving digital payments ecosystem.

Just as the Central Bank announced new security restrictions on Pix, capping transactions at R$ 200 (≈$35 USD) on unregistered devices with a R$ 1,000 daily limit to combat fraud, it also issued Resolution No. 561, an outright ban on using stablecoins and cryptocurrencies for cross-border payment settlements.

The measure to limit Pix’s transfer amount by the Central Bank of Brazil aims to increase security and reduce fraud, especially in cases of account hacking and digital scams.

On the other hand, while individual crypto trading remains permitted, FinTechs and eFX providers can no longer use Bitcoin or stablecoins as the back-end rail for international remittances starting October 1, 2026.

Brazil's regulator is drawing a line for crypto to exist in the market, but not as an eFX settlement infrastructure.

Scroll down to discover the rest of the payments’ big shifts below👇 See you tomorrow!

Cheers,

INSIGHTS

📰 Central Bank Digital Currency (CBDC) by DashDevs. Written by Artur Nesterenko, the piece explains that CBDCs are state-issued digital currencies designed to function as regulated digital cash or settlement infrastructure. It outlines their key use cases, differences from stablecoins and bank money, and the strategic trade-offs, highlighting their growing relevance as a foundational layer for payments, wallets, and financial infrastructure.

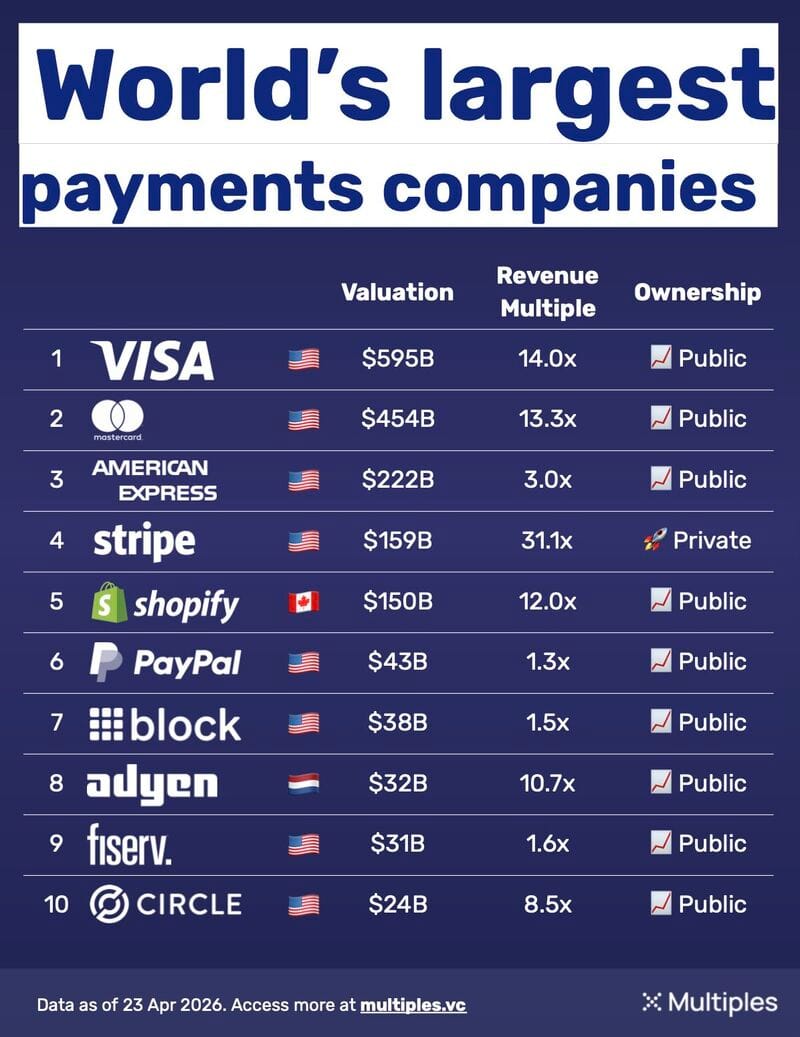

🌍 The world’s top 10 payments companies are worth over $𝟭.𝟲 𝗧𝗥𝗜𝗟𝗟𝗜𝗢𝗡 🤯

And two names dominate the entire industry👇

NEWS

🇦🇪 Botim money and Mastercard expand multi-year agreement to broaden eligibility for digital card payments in the UAE. botim money cards are available without a minimum salary threshold, widening eligibility across the UAE’s diverse resident base and supporting everyday payment access for more users, while keeping the programme aligned with standard service practices.

🇺🇸 Stablecoin startup Rain is worth $1.95 billion and plans to issue Mastercard cards to woo institutional customers. Rain said it was working with Mastercard to explore how to settle payments with the public company using stablecoins, or cryptocurrencies pegged to real-world assets like the U.S. dollar.

🇧🇷 Pix will have a maximum limit of R$ 200 after a change announced by the Central Bank to combat fraud. Transfers from unrecognised devices will be temporarily limited, while banks like Nubank, Itaú Unibanco, and Caixa Econômica Federal can now apply precautionary blocks on suspicious transactions for up to 72 hours.

🇧🇷 Brazil's central bank bans stablecoin and crypto settlement in cross-border payments. The ban applies to FinTechs and payment firms, closing the back-end payment rail for cross-border flows, but individual crypto investors can still buy and hold assets.

🇺🇸 Tether posts $1.04 billion Q1 profit, reaches $8.23 billion reserve buffer. The issuer of the USDT stablecoin said its total assets are just under $192 billion against liabilities of slightly more than $183.5 billion, with most reserves in U.S. government-backed instruments.

🇨🇦 Francisco Partners is in talks to buy payments company Moneris from its owners, Royal Bank of Canada and Bank of Montreal, in a deal that could value the business at up to $2 billion. The potential sale reflects a broader trend of banks exiting merchant payments as FinTech players reshape the industry.

🇫🇷 Worldline completes divestment of Electronic Data Management to SIX. This operation marks another step in the Group’s strategic refocus on core European synergistic payment activities, enabling Worldline to simplify operations and optimize resource allocation, in line with its North Star transformation plan.

🇿🇦 Stitch adds BNPL to payments platform. BNPL allows customers to split payments into two to six instalments, with the repayment schedule chosen at checkout. Merchants receive full payment within 24 hours of a transaction, rather than waiting for instalment repayments to complete over time.

🇺🇸 Western Union selects Fireblocks to power its first stablecoin, USDPT. Fireblocks will provide the wallet, settlement, and financial operations infrastructure for Western Union's digital dollar, extending access and creating the foundation for a broader set of financial services to consumers in the Philippines and Bolivia, with global rollout planned through 2026. Additionally, USDPT has been rolled out on Solana. The stablecoin is designed to operate within real‑world payment systems, combining blockchain‑based settlement with Western Union’s global compliance, risk and distribution capabilities.

🇦🇪 Telr launches Google Pay, enabling faster, seamless, and secure payments for all Telr merchants. Built for speed and designed for trust, Google Pay enables customers to complete transactions instantly using cards securely stored in their Google Wallet, eliminating the need to re-enter payment details. It delivers a faster, smoother payment experience.

🇨🇦 Tetra Digital Group launches CADD, Canada’s first CAD-backed stablecoin issued by a financial institution. This marks a national first for digital asset infrastructure in Canada by enabling Canadian dollars to move on blockchain rails under a financial services regulatory framework.

🇫🇷 Circle France receives approval to offer crypto-asset services under MiCA. This approval enables Circle France to offer custody and transfer services for crypto-assets related to the stablecoins it issues, USDC and EURC. As a result, Circle France can now provide these services to customers across the European Economic Area.

🇺🇸 AI-driven Long Lake agrees to take Amex GBT off market in $6.3bn deal. Backed by General Catalyst and Alpa Wave, the acquisition aims to accelerate AI-driven innovation in business travel, while American Express will exit its stake but retain brand licensing.

GOLDEN NUGGET

𝐋𝐨𝐜𝐚𝐥 or 𝐠𝐥𝐨𝐛𝐚𝐥 𝐜𝐚𝐫𝐝𝐬: how to choose the right strategy 👇Created by Arthur Bedel 💳 ♻️

Most companies frame this as a binary choice.

It is not.

Local and global cards do not compete with each other.

They solve different problems at different stages of the business — and knowing which to use, and when, is what defines a smart card strategy.

Local cards are built for depth.

They adapt to local regulations, support domestic payment schemes, and align with local payment habits — installments, differentiated interest rates, country-specific tax structures.

The result: greater customization and stronger adoption in markets where standardized solutions struggle to compete.

Global cards are built for reach.

They enable seamless cross-border #Payments, operate under international standards, and deliver a consistent user experience across geographies — which makes them ideal for validating new markets before committing to a full local entity.

The result: faster market exploration and growth, with portability built in.

And in practice, very few companies that scale regionally stay on a single model.

The reality is hybrid. Local captures domestic volume. Global enables fast expansion.

The challenge has always been infrastructure — keeping both models running without duplicating complexity or fragmenting operations.

But here is the bigger shift happening across #Fintech right now.

The future is multi-rail.

#Payments no longer rely on a single system. Cards, real-time rails, and #Stablecoins all coexist — and each has its ideal use case.

What is interesting is that cards remain at the core of all of it.

Why? Because they are the bridge.

They translate stablecoin balances into real-world spending power. They enable BNPL adoption to scale across the existing merchant network. They connect emerging financial systems to the real economy.

The discussion is no longer which rail replaces which.

It is how they combine to deliver better experiences and lower costs.

Pomelo is making this real for #LATAM — letting companies launch local cards across the region through a single integration, while supporting global card programs and emerging rails from the same architecture.

One partner. Every market. Local depth + regional speed.

The companies that win the next decade in LATAM won't choose between local and global.

They'll build for both — and stay flexible enough to plug in whatever comes next.

Are you building local-first, global-first, or hybrid?

Source: Pomelo

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()