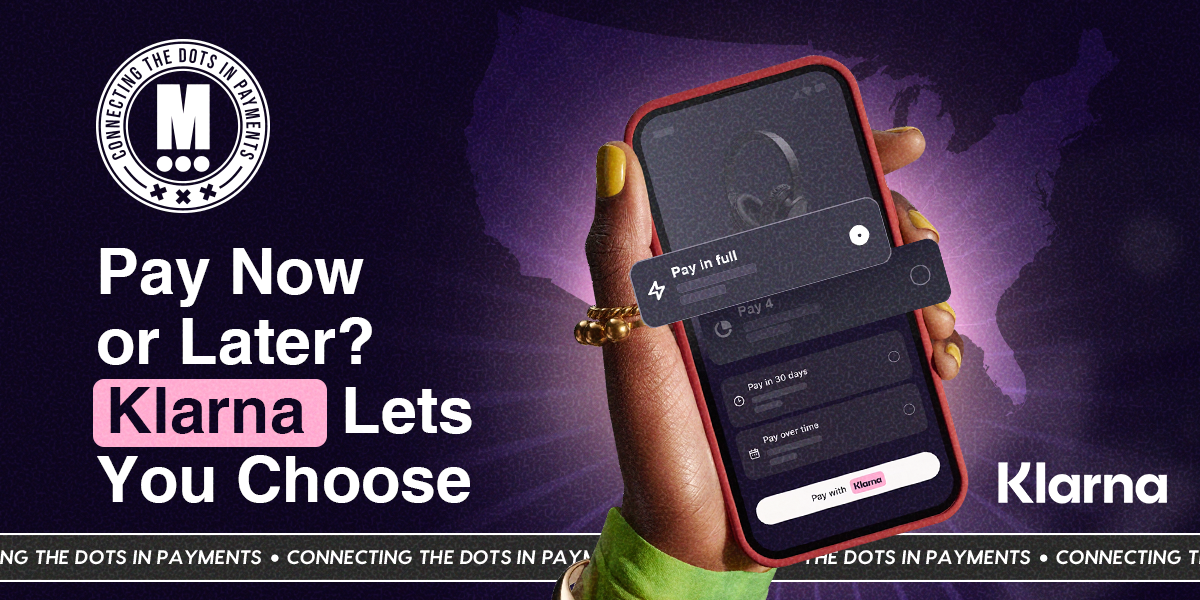

Klarna Pilots Klarna Card with Visa — Pay Now or Later, All in One

Hey Payments Fanatic!

Klarna has launched the pilot of Klarna Card in the U.S, a flexible new debit-first card powered by Visa’s Flexible Credential and issued by WebBank. The card lets users pay immediately or later — online or in-store — at over 150 million merchants globally.

Unlike traditional credit cards, Klarna Card is built to avoid debt and hidden fees, putting real payment choice in the hands of consumers.

“We consistently hear from consumers that they want the freedom to choose how and when to pay - whether that’s paying now with debit or spreading the cost over time,” said David Sandstrom, CMO at Klarna. “This is the future of everyday banking — smart payments for smarter shoppers.”

With over 5 million already on the waitlist, Klarna is currently testing the product in the U.S. ahead of a broader rollout in the U.S. and Europe later this year.

The card includes:

• An FDIC-insured wallet

• Real-time transfers and deposits

• Seamless integration with Pay in 4 and Pay Later

“Millions of people around the world have embraced the choice and control offered by Visa’s Flexible Credential, and we’re delighted to extend this to even more U.S. consumers, as well as bringing it to Europe for the first time,” said Mathieu Altwegg, SVP at Visa Europe.

With this launch, Klarna continues its evolution into a global, digital-first neobank, combining spending, saving, and borrowing into a single, intuitive experience.

Read more global payment industry updates below 👇 and I'll be back with more tomorrow!

Cheers,

NEWS

🇬🇧 Payment insights that move the travel industry forward by CellPoint Digital. CellPoint's Insight Hub serves as a curated resource designed for industry executives, product leaders, and innovators shaping the future of travel commerce. It draws on the team’s collective expertise to offer practical insights into how orchestration, optimization, and operational control can drive tangible business outcomes.

🇳🇱 Mollie's growth increases by 30% in 2024. Gross profit rose by 30% to €115 million. Revenue also saw a significant increase of 28%, reaching a total of €214 million. This growth was driven in part by a clear product focus and continued international expansion, while operating expenses remained stable throughout the year.

🇪🇸 PagoNxt Payments Powers Getnet: enabling multi-currency payments across 140+ currencies. Integrating PagoNxt Payments’ FX Engine has significantly enhanced Getnet’s capabilities. This allows Getnet to offer merchants a more predictable and transparent FX experience, reducing operational complexity while unlocking new revenue streams.

🇩🇪 Deutsche Bank and Mastercard partner to enhance merchant solutions with open banking payments. The partnership empowers merchants to leverage R2P as a preferred payment method, giving consumers the ability to authorize payments directly from their bank accounts with real-time processing and immediate confirmation.

🇬🇧 Revolut pushes into crypto derivatives, skirting UK ban on retail sales. After reporting record profits earlier this year, Revolut is now looking to expand its crypto offering. Derivatives are financial products that allow traders to speculate on the future price of assets without having to own assets directly.

🌏 Nomupay has raised $40 million and entered into a partnership with Japanese payments solution firm SB Payment Service (SBPS). The deal is at a valuation of $290 million. The investment solidifies Nomupay’s intention to become the number one payment platform in Asia.

🇺🇸 Google Wallet is losing access to PayPal. Google says it will stop supporting the payment method and automatically delete linked PayPal accounts on June 13th, 2025. Users will have to manually add a credit card, debit card, or bank information if they want to keep using the app.

🇵🇱 HandGo by Autopay, Poland’s first palm-authenticated shopping. HandGo is an innovative biometric palm-authenticated shopping system. It is a very intuitive solution using a special scanner in lieu of a card payment terminal. Read more

🇦🇪 RLUSD is approved by the Dubai Financial Services Authority as a recognised crypto token. This recognition allows Ripple to integrate RLUSD into its DFSA-licensed flagship payments solution, combining the stability of a trusted digital dollar with a scalable, blockchain-based infrastructure and Ripple’s extensive global payout network.

🇺🇸 Visa appoints Andrew Torre as President of Value-Added Services. In his new role, Mr. Torre will be responsible for designing, developing, and delivering Visa’s VAS portfolio of products and solutions. He will be based in San Francisco and take on this role effective immediately.

🇬🇧 Zilch partners with Visa for a physical card. The physical card opens up flexibility to millions of customers. Customers will have the ability to shop anywhere in the world that Visa is accepted, online or offline, with the same flexible repayment options.

🇬🇧 Powering smarter pay-by-bank in the UK with Visa and Plaid. The A2A solution brings together real-time authentication, persistent consent, instant settlement, and Visa’s trusted protections to support everything from subscription billing to utility payments.

🇲🇽 Bitso introduces new service enabling U.S. dollar transfers for users in Mexico and Argentina. The service also allows for USD withdrawals to U.S. accounts from the app under the Withdrawals menu. Keep reading

🇬🇧 AllPay launches Dosh prepaid card in the UK. Dosh removes common barriers to entry, such as rigid ID and address checks, offering a more inclusive route to financial services for people often left behind by the mainstream, from those new to the UK to individuals in temporary housing.

🌍 Thunes expands direct global network into Denmark, Norway, and Sweden. This broadens Thunes’ reach into the Nordic region, empowering Members of the Thunes Direct Global Network with faster cross-border payment solutions for both consumer and business transactions.

🇮🇳 Wise secures IPA for cross-border payment aggregator in India. By securing the licence, Wise is set to be able to facilitate higher transaction limits of up to USD 0.29 (25 lakh) for freelancers and businesses receiving cross-border payments through the company’s international account details capability.

🇬🇧 Wise partners with Opna to drive climate resilience with high-impact carbon removal. Through this collaboration, Wise has committed £500,000 to high-integrity nature-powered carbon removal projects across Wise’s key growth markets in Latin America (LatAm) and Asia-Pacific (APAC).

🇳🇱 Utrecht-based FinTech startup SurePay secures growth investment. It will use the fresh funding to further expand its payment verification and fraud prevention solutions and to broaden its geographic presence across Europe and beyond, also to support the company’s goal to continue serving its blue-chip customers effectively.

🇺🇸 PayPal enhances popular online credit offering with new physical card for in-store use. When using the new physical card, customers will also have access to a limited-time offer to pay for travel purchases over six months with promotional financing and no minimum spend.

🇺🇾 Uruguay’s DLocal agrees to buy AZA Finance in Africa Push. The transaction, which is subject to regulatory approval, was announced in a statement. The deal is valued at about $150 million. Keep reading

🇩🇪 Nova Wallet partners with Mercuryo to launch Polkadot Mastercard Debit Card. It was designed to give customers the ability to pay with their crypto assets for purchases. Users can top up their cards using Polkadot tokens, providing a unique way of spending for everyday purchases using DOT tokens that are converted into fiat.

GOLDEN NUGGET

Welcome to 𝐓𝐡𝐞 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐀𝐜𝐚𝐝𝐞𝐦𝐲 by Checkout.com — Episode 16 👋 Created by Arthur Bedel

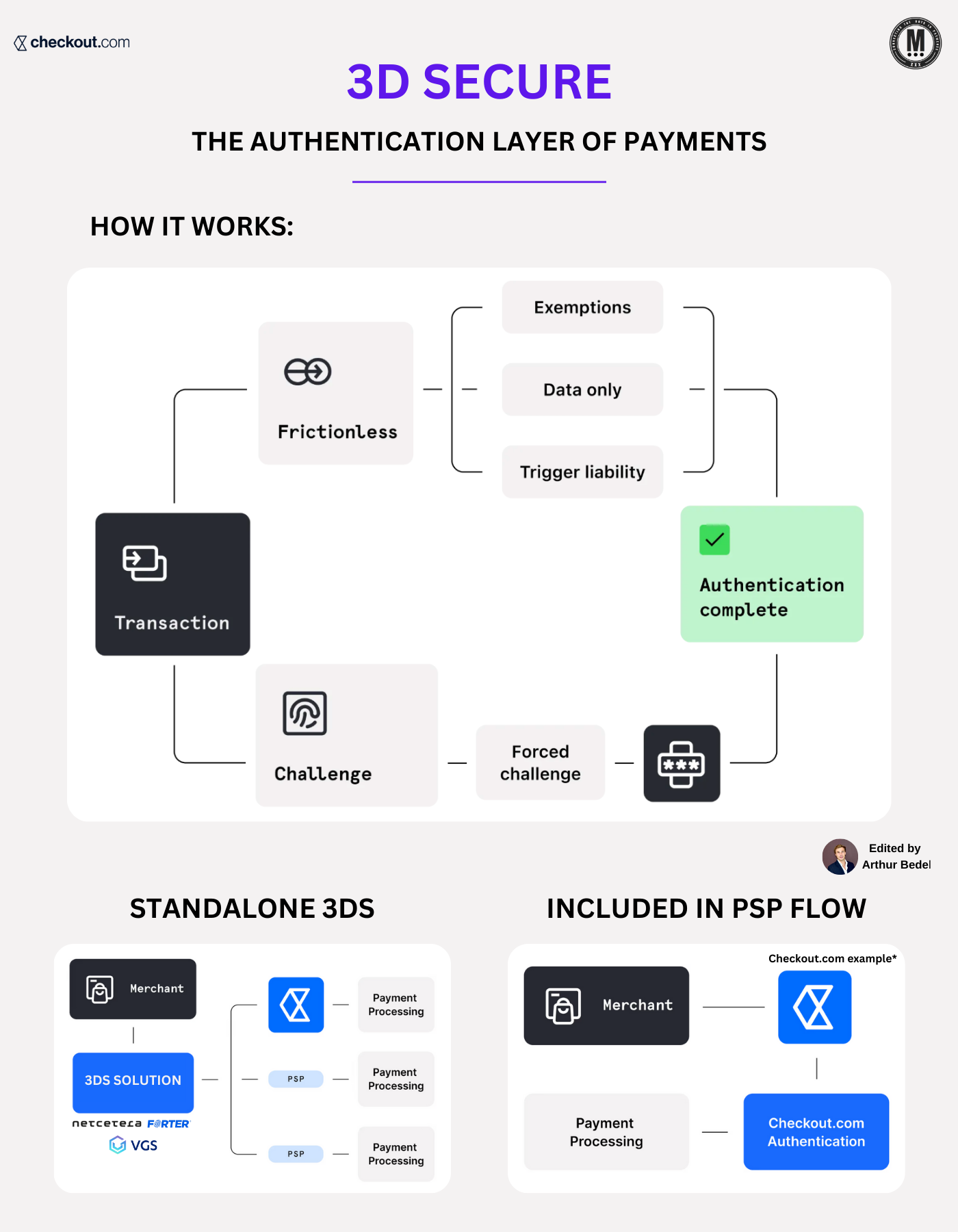

𝟑𝐃 𝐒𝐞𝐜𝐮𝐫𝐞 — The Authentication Layer in Card-Not-Present Transactions

3D Secure (3DS) is a security protocol developed by EMVCo to authenticate online cardholders in real time. It facilitates risk-based authentication between the issuer, merchant, cardholder, and Access Control Server (ACS)—creating an added layer of trust in card-not-present (CNP) transactions.

𝐇𝐨𝐰 𝐝𝐨𝐞𝐬 𝟑𝐃 𝐒𝐞𝐜𝐮𝐫𝐞 𝐰𝐨𝐫𝐤?

3DS dynamically adapts to the transaction risk profile using one of two core flows:

1️⃣ 𝐅𝐫𝐢𝐜𝐭𝐢𝐨𝐧𝐥𝐞𝐬𝐬 𝐅𝐥𝐨𝐰

✔ No customer interaction

✔ The issuer’s ACS validates the cardholder silently using contextual signals (device ID, IP, geolocation, past behavior)

✔ Ideal for low-risk transactions and returning users

2️⃣ 𝐂𝐡𝐚𝐥𝐥𝐞𝐧𝐠𝐞 𝐅𝐥𝐨𝐰

✔ Issuer actively authenticates the cardholder

✔ Methods may include OTP, face ID, fingerprint, or app push notification

✔ Used when risk is elevated or regulatory thresholds require stronger SCA (e.g., PSD2 in Europe)

𝐖𝐡𝐚𝐭 𝐢𝐬 𝐋𝐢𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐒𝐡𝐢𝐟𝐭?

When 3DS is applied (and the issuer approves the authentication), liability for fraud-related chargebacks shifts from the merchant to the issuer.

This is especially critical for:

→ High-value CNP transactions

→ Cross-border payments

→ SCA-mandated regions (e.g., EU, UK, India)

𝐒𝐭𝐚𝐧𝐝𝐚𝐥𝐨𝐧𝐞 𝟑𝐃𝐒 𝐯𝐬. 𝐏𝐒𝐏-𝐞𝐧𝐚𝐛𝐥𝐞𝐝 𝟑𝐃𝐒

📌 Standalone 3DS - Merchants directly integrate with a 3DS provider or ACS (VGS, Forter...)

→ Full control over routing, rules, and orchestration

→ More complex setup, ongoing maintenance, and liability handling

→ Best for technology-driven & enterprise merchants

📌 PSP-enabled 3DS - the PSP(Checkout.com, Adyen...) manages the 3DS flow

→ Simpler integration, streamlined performance

→ Embedded in the PSP’s payment flow

→ Built-in liability management and reporting

→ Less granular control over ACS selection or custom rule logic

→ Best for traditional merchants or start/scale-ups.

𝐖𝐡𝐲 𝐌𝐞𝐫𝐜𝐡𝐚𝐧𝐭𝐬 𝐬𝐡𝐨𝐮𝐥𝐝 𝐜𝐚𝐫𝐞

► Seamless user experience with risk-based friction reduction

► Increased authorization rates through dynamic routing

► Fraud reduction + chargeback liability protection

► Regulatory compliance with PSD2, RBI, and global SCA mandates

Source: Checkout.com

Want your message in front of 100.000+ FinTech fanatics, founders, investors, and operators?

Shoot me a message on LinkedIn or send me an e-mail.

Comments ()